As the cost of higher education continues to rise globally, numerous students find themselves grappling with the question of how to finance their dreams of a college or university degree. In the vast landscape of educational funding, two primary mechanisms stand out: student loans and scholarships.

While both serve the critical purpose of helping students afford their education, they have stark differences that are crucial to understanding before making decisions on how to fund your studies.

This comprehensive guide will delve into the intricate details of both student loans and scholarships, addressing the fundamental question – “How is a Student Loan Different From a Scholarship?”

Whether you are a high school student contemplating your college funding options, a current college student considering how to finance the rest of your academic journey, or a parent seeking to understand the best ways to support your child’s education, this guide will offer valuable insights to help you navigate the path to educational financing.

Student Loans

As we embark on this journey of understanding the financial support mechanisms available for higher education, let’s start with the concept of student loans.

What is a Student Loan?

Student loans aim to help students pay for the costs of their higher education, such as tuition, books, supplies, and living expenses. It’s crucial to remember that student loans are a debt that entails paying interest on the amount borrowed. Interest serves as a cost for borrowing money. While student loans can provide essential financial assistance to people who might otherwise find it difficult to pay for education, they also place a financial strain on graduates because the loans must be returned over a predetermined period of time.

In the following sections, we will explore the different types of student loans, their unique features, and the key differences in interest rates, fees, and repayment options.

Understanding the fundamentals of student loans is crucial, as it empowers students and parents to make informed decisions about funding for higher education. So, whether you’re considering taking out a student loan or already have one and want to understand it better, keep reading as we delve deeper into this important financial tool.

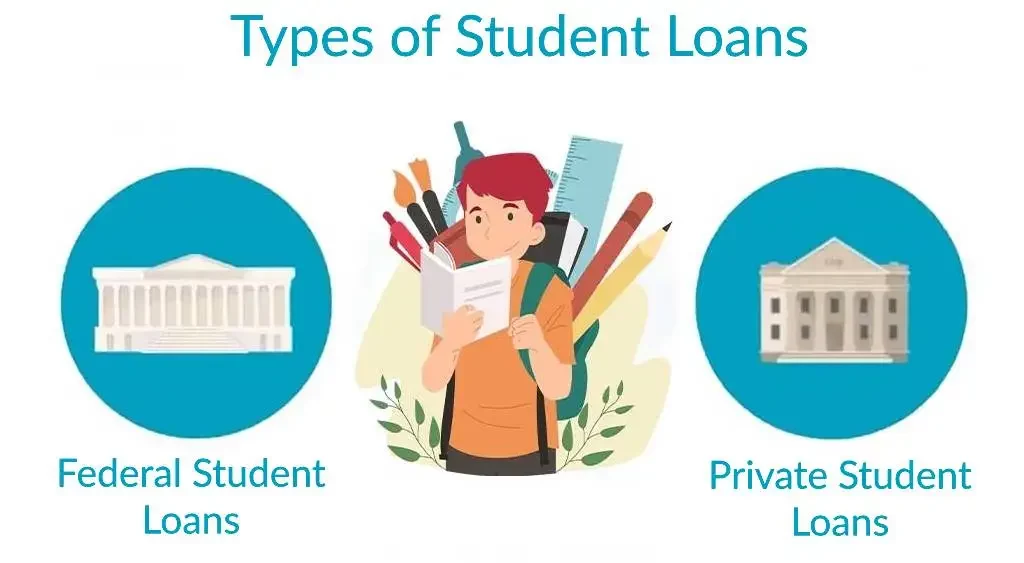

Types of Student Loans

Making informed decisions about how to pay for your education requires a thorough understanding of the various types of student loans. Federal student loans and private student loans are the two main categories. Each type has unique regulations, interest rates, advantages, and disadvantages.

Federal Student Loans

Loans that provide lower, fixed interest rates and more lenient repayment terms than private loans are frequently regarded as the best choice for students. Additional advantages of federal loans include opportunities for loan forgiveness in certain professions and income-driven repayment plans.

Direct Subsidized Loans:

Students in their undergraduate years who can prove they have a genuine financial need can apply for one of these loans. The U.S. Department of Education pays the interest on these loans while the student is enrolled in their academic program and for a specific amount of time after finishing their studies. The educational institution sets the maximum borrowing amount.

Direct Unsubsidized Loans:

Both graduate and undergraduate students can access these loans, regardless of their financial need. In contrast to subsidized loans, the borrower must always pay the interest on these loans.

PLUS Loans:

These credit-based loans are available to parents of dependent undergraduate students as well as graduate or professional students.

Private Student Loans

In contrast, private student loans are non-federal loans provided by various lenders such as banks, credit unions, government agencies, or higher education institutions. These loans generally come with higher interest rates and less flexible repayment terms compared to federal loans. Additionally, private loans may have variable interest rates, which means they can fluctuate either upwards or downwards over time.

When federal loan options have been exhausted, and additional funding is still required to pay for education costs, private student loans are frequently used. Before accepting a private loan, it is crucial to read the fine print because the terms and conditions differ greatly between lenders.

We will examine how these loans vary in terms of interest rates, costs, and repayment options in the sections that follow. We’ll also go over each option’s benefits and drawbacks to help you choose what will work best for you.

Remember, while student loans can be a useful tool in financing your education, it’s important to borrow only what you need and what you expect to be able to repay in the future.

Interest Rate, Fee, and Repayment Options Variations

Understanding the financial details of student loans, such as interest rates, fees, and repayment options, is critical when deciding which loan best suits your needs.

Federal student loans have fixed interest rates, which are frequently less expensive than those of private loans. This indicates that the interest rate won’t alter throughout the loan’s term. In addition, each loan disbursement is subject to loan fees, which represent a percentage of the loan amount. Federal student loans‘ adaptable repayment options are one of their main benefits.

They provide alternatives such as income-driven repayment, which adapts your monthly payment according to your income and the size of your family.

On the other hand, the interest rates on private student loans can be either fixed or variable. Variable rates may start lower than fixed rates but can increase over time, causing your total loan cost to rise. Private loans may also come with fees, and their repayment options are often less flexible than federal loans. Some may require repayment while you’re still in school, and they typically do not offer income-driven repayment plans.

Pros and Cons of Student Loans

Student loans, like any financial product, come with their advantages and disadvantages.

Pros:

- They provide students with access to higher education who might not have otherwise had the means to do so.

- Federal student loans are available, and they come with lower, fixed interest rates and flexible repayment options.

- They can help build credit when payments are made consistently and on time.

Cons:

- Upon graduation, the repayment of student loans, including the accrued interest, can impose a significant financial burden.

- The presence of substantial loan balances may affect your eligibility for obtaining other forms of credit, such as mortgages or auto loans.

- Furthermore, defaulting on a student loan can have adverse consequences on your credit history and potentially lead to wage garnishment.

How to Get a Student Loan

A few crucial steps are required to obtain a student loan:

- Completing the FAFSA: To assess your eligibility for federal student loans and various forms of financial aid, please complete the designated form promptly. Completing the form expeditiously enhances your chances of qualifying for financial assistance to the fullest extent possible.

- Verify the financial aid offer. If federal student loans are available to you, your school will include them in the package. To determine the types and amounts of loans you qualify for, carefully read this offer.

- Accept your loans: If you decide to take out federal student loans, you must do so through the financial aid department of your school.

- Complete loan counseling and sign a promissory note: Before receiving your loan, you’ll need to undergo loan counseling to understand your obligations as a borrower and sign a promissory note agreeing to the terms of the loan.

- Apply for private student loans: If your federal loan options have been exhausted and you still need additional funding for school, you can submit an application for a private student loan directly with a lender.

Scholarships

Now that we’ve explored the landscape of student loans, let’s shift our focus to another form of educational funding that doesn’t require repayment – scholarships.

How Scholarships Work

In essence, scholarships are grants of free money given to students to assist with the cost of their education. Scholarships are a desirable option for students looking to finance their education because, unlike loans, they do not need to be repaid. They frequently take into account a number of factors that reflect the ideals and goals of the award’s founder or donor.

Scholarships can come from many different sources, including schools, private organizations, nonprofits, religious groups, businesses, and local communities. They can be used to cover living costs occasionally, as well as tuition, board, and books.

Depending on the scholarship, a different amount may be given. While some scholarships only offer a single award, others are renewable and give students money each semester or academic year. Scholarships are generally sent directly to your school and applied toward any tuition, fees, room and board, and other school charges. Any money left over is paid to you for other educational expenses.

Scholarships are an excellent way to pay for school because they provide students with free money that doesn’t have to be repaid. However, they often require some work on the student’s part, such as applying for a scholarship, meeting certain academic criteria, or writing an essay.

In the following sections, we will delve deeper into the different types of scholarships, their pros, and cons, and provide a guide on how to secure them. Whether you’re just starting your scholarship search or looking for ways to boost your scholarship portfolio, this guide will provide the insights you need to navigate the scholarship process effectively.

Types of Scholarships

As we delve deeper into the world of scholarships, it’s important to understand that not all scholarships are created equal. They come in various forms and are awarded based on different criteria. Here, we’ll explore some of the most common types of scholarships: merit-based, need-based, athletic, and creative scholarships.

Merit-Based Scholarships

Merit-based scholarships are awarded to students who have shown exceptional ability in one or more areas of their academic or extracurricular activities. These can be based on academic achievements, leadership roles, community service, or other talents. The main purpose of these scholarships is to reward students for their hard work and dedication in these areas. To maintain a merit-based scholarship, students are often required to meet certain academic standards, such as maintaining a specific grade point average.

Need-Based Scholarships

These grants aim to level the playing field and open up education to everyone, regardless of their financial situation. The Expected Family Contribution (EFC), which is the amount of money a family is expected to contribute to education in the United States of America, is typically calculated using the FAFSA (Free Application for Federal Student Aid).

Athletic Scholarships

For students who excel in sports, athletic scholarships are available. These scholarships are frequently given out by colleges and universities to entice elite athletes to join their sports teams. The competition for athletic scholarships can be fierce, and those who receive them are typically expected to play their sport in college.

Creative Scholarships

Creative scholarships are designed for students who have demonstrated talent in a creative field such as art, music, dance, writing, or film. These scholarships can help support students pursuing degrees in these fields. To apply for a creative scholarship, students typically need to submit a portfolio or samples of their work.

In each of these categories, the amount of the scholarship and the application process can vary significantly. It’s important to research each scholarship thoroughly and ensure you meet all the eligibility requirements before applying. In the next sections, we will discuss the pros and cons of scholarships and provide tips on how to secure them. Remember, scholarships can significantly reduce the financial burden of higher education, so it’s worth investing time and effort into the application process.

Pros and Cons of Scholarships

Scholarships, as a financial resource for education, come with their set of advantages and potential drawbacks. Let’s explore these in more detail.

Pros:

- They Do Not Need to Be Repaid: Unlike loans, scholarships are essentially free money that doesn’t need to be repaid. This feature significantly reduces the financial burden post-graduation.

- Encourages Achievement: Merit-based scholarships incentivize academic or extracurricular achievement, pushing students to strive for excellence.

- Increases Access to Education: Scholarships, especially need-based ones, can make higher education accessible to students who might otherwise not afford it.

Cons:

- Highly Competitive: Scholarships, particularly those with substantial awards, can be highly competitive, with hundreds or even thousands of students vying for a single award.

- Application Process Can Be Rigorous: Applying for scholarships often requires significant time and effort, including gathering documents, writing essays, or preparing a portfolio.

- Maintenance Criteria: Some scholarships require recipients to maintain certain academic standards or fulfill specific obligations, which can add pressure on students.

How to Get a Scholarship

- Start Early: The earlier you start your scholarship search, the more options you’ll have. Some scholarship deadlines are as early as a year before college starts, so start your search early in high school.

- Use Scholarship Search Engines: Websites like Fastweb, Cappex, and Chegg Scholarships can help you find scholarships that match your specific qualifications.

- Apply for Local Scholarships: Check with your school’s guidance office or your local community organizations for scholarship opportunities. These scholarships are less competitive than national ones.

- Meet All the Requirements: Make sure you meet all the eligibility requirements before you spend time applying for a scholarship.

- Pay Attention to Details: Many scholarship applications are discarded because of errors or incomplete information. Make sure to proofread your application and include all necessary documents.

- Write a Strong Essay: If the scholarship application requires one, make sure to proofread and carefully write it. Take your time to write a compelling and captivating essay because it can help you stand out from other applicants.

- Don’t Give Up: It might take a lot of time and be depressing to apply for scholarships. But keep in mind that every scholarship you receive is money you don’t have to pay back. Long-term results can really show the value of your work.

Differences between Student Loans and Scholarships

Its essential to understand how is a student loan different from a scholarship as we travel the financial path of higher education. While both are methods to finance education, they function quite differently. Let’s break down these differences based on purpose, repayment, eligibility, availability, amount, and impact on the future.

Purpose

Both student loans and scholarships serve the same primary purpose: to finance education. However, student loans are typically used to cover the bulk of education costs, including tuition, room and board, and other fees. Scholarships, on the other hand, are often geared towards covering specific costs, such as tuition or books, or providing financial support to students from certain backgrounds or with certain skills.

Repayment

Repayment is one of the key distinctions between scholarships and student loans. Interest must be paid on all student loans, including federal and private ones. Serious financial repercussions may result if you don’t do it. Scholarships, however, are essentially gifts that do not need to be repaid.

Eligibility

Scholarships and student loans have different eligibility restrictions. Students must submit the FAFSA, enroll in a degree or certificate program that has been authorized, and make sufficient academic progress in order to be eligible for federal student loans. On the other hand, private loans frequently need additional requirements, such as going through a credit check. Scholarships offer a wide range of requirements for applicants, which frequently include things like academic achievement, financial necessity, the field of study of choice, or personal traits.

Availability

While federal student loans are widely available to most students attending accredited institutions, private loans and scholarships can be more limited. Private loans often require a good credit history or a co-signer, and scholarships are typically competitive, with limited awards available.

Amount

The amount of money you can receive varies as well. Federal student loans have annual and lifetime limits, but these are generally high enough to cover most educational expenses. Private loans can often fill any gaps left after federal loans, up to the cost of attendance. Scholarships can range from small amounts to cover books or supplies to full-ride scholarships covering all costs of attendance.

Impact on Future

Student loans, while offering the opportunity for higher education, can impact your financial future. Loans can lead to long-term debt and affect your credit score and ability to borrow in the future. Scholarships, being debt-free, do not have this impact.

Concluding Thoughts

Navigating the world of higher education funding can be a complex journey. Understanding the differences between student loans and scholarships is crucial to making informed decisions about financing your education.

While both student loans and scholarships aim to aid students in pursuing their educational dreams, they are fundamentally different in their purpose, repayment terms, eligibility requirements, availability, amount, and impact on future financial health.

Student loans, although readily available, must be repaid with interest and can influence your long-term financial situation. Scholarships, on the other hand, provide a monetary gift to support education based on various criteria and do not need to be repaid, offering a financially healthier alternative. Regardless of the route you choose, it’s vital to have a versatile understanding of how is a student loan different from a scholarship.

In the end, remember that investing in your education is one of the most important investments you can make in yourself. Being well-informed about ‘how is a student loan different from a scholarship’ is the first step in this significant journey toward your future.

Frequently Asked Questions (FAQ)

Can I receive a scholarship as well as a student loan?

Indeed! Numerous students opt for a combination of scholarships, grants, and student loans to finance their higher education expenses. Scholarships and grants can significantly reduce the amount of money one needs to borrow. It is crucial to explore all available avenues for “free money,” such as scholarships and grants, before resorting to student loans.

What should I do if I am struggling to repay my student loan?

If you’re having trouble repaying your student loan, don’t panic, but don’t ignore the situation either. Reach out to your loan servicer immediately. You can choose from deferment, forbearance, or income-driven repayment plans if you have federal student loans.

There are fewer options if you have private student loans, but your lender might still let you temporarily reduce your payments. Recall that it’s crucial to communicate with your lender because failing to do so could result in bigger problems, such as default.

What distinguishes grants from loans from scholarships?

Grants, loans, and scholarships all provide funding for education, but they operate differently.

- Grants are typically given based on need and don’t have to be paid back. Governmental agencies, educational institutions, and nonprofit organizations frequently offer them.

- Borrowed money is what is used for loans, and interest is always charged. The resources of the government, as well as private lenders, can supply them.

- Typically, scholarships are non-repayable awards given based on need or merit. They may be offered by various companies, organizations, or individuals.