Rent is a big part of most people’s budgets, and with rising housing costs in many areas, finding a balance between affordability and comfort is more important than ever. You may find yourself asking, how much of your income should go to rent? Whether you’re just starting your rental journey or reconsidering your current setup, determining the right amount to spend on rent can help you avoid financial stress while keeping room for other goals.

In this guide, we’ll explore common guidelines like the popular 30% rule, break down factors that influence rent affordability, and even cover smart ways to save. Let’s dive in and uncover how you can make the best decision on rent for your financial health and lifestyle.

Understanding Rent Allocation Guidelines

Most experts suggest that rent shouldn’t consume more than 30% of your gross monthly income, but where did this rent allocation rule come from? The concept originated in the U.S. in the 1980s and was primarily used as a metric in housing assistance programs to ensure families could cover other essential expenses.

But today, many renters are in high-cost markets, juggling student debt, and facing unique financial situations that can make rigid adherence to a 30% rule unrealistic. So, how much of your income should go to rent? Here’s a breakdown of the most common rent guidelines and what they imply:

The 30% Rule

This traditional benchmark suggests capping rent at 30% of your gross monthly income, which is your income before taxes. For example, if you earn $4,000 monthly, 30% means your rent should ideally be $1,200 or less. This amount would, in theory, leave you with 70% of your income for other essentials, savings, and discretionary spending.

The 50/30/20 Rule

A modern twist on budgeting, this rule suggests allocating 50% of your income to essentials like rent, groceries, and utilities, 30% to discretionary spending, and 20% to savings or debt payments. In this model, you have flexibility: if your rent and other essentials fit within the 50%, you’re on track.

The Roommate Rule

For those open to sharing their space, the roommate rule suggests splitting costs with another person, ideally reducing the share of rent to around 15-20% of each renter’s gross income. Living with a roommate is often the easiest way to keep costs low while still enjoying a spacious and desirable area.

Each of these rent allocation rules offers a framework, but they’re just starting points. While it’s valuable to keep these in mind, don’t be afraid to adjust based on your needs and location.

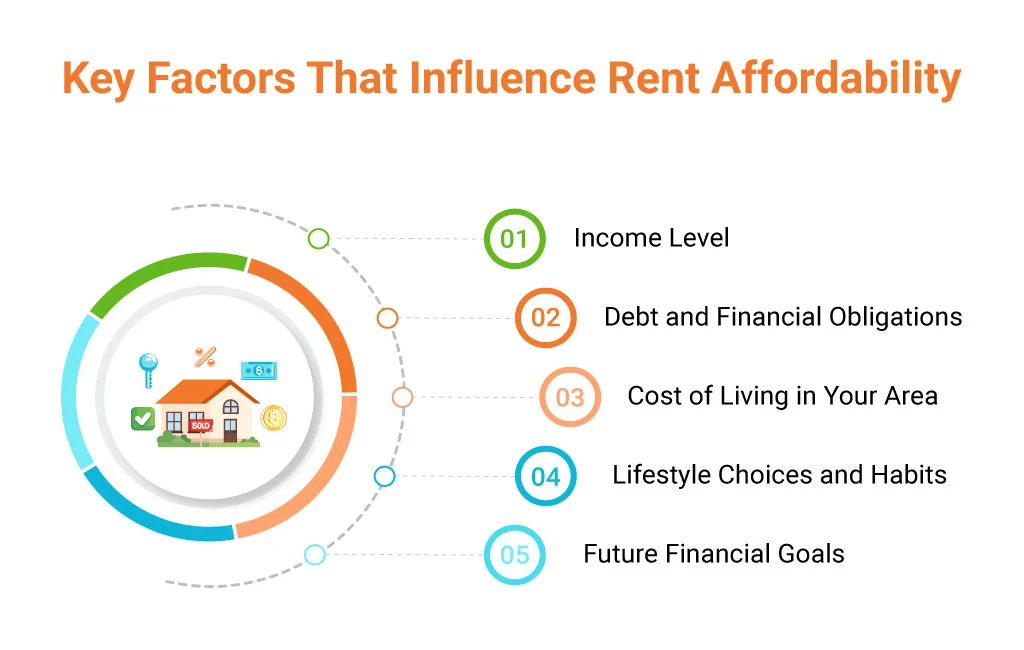

Key Factors That Influence Rent Affordability

Deciding how much of your income to allocate to rent goes beyond simple budgeting rules. Here are the main rent cost factors to consider when assessing what’s truly affordable:

Income Level

Your gross monthly income is the starting point for any budget, but the real focus should be on what’s comfortable to spend after taxes and other deductions. Knowing how much of your income should go to rent is key.

For example, if you make $5,000 a month, you can likely afford more rent than someone earning $2,500. Take-home pay and any other stable income sources are essential to consider, as they form the foundation of what’s feasible.

Debt and Financial Obligations

Debt can heavily influence how much you can allocate toward rent. Monthly payments for student loans, car loans, or credit cards directly reduce what’s left for housing. Financial exceptions may apply, as a person with little or no debt may find they have more flexibility, while someone with high debt might need to keep rent below the standard 30% guideline to maintain financial stability.

Cost of Living in Your Area

Rent prices vary widely by location. In high-cost cities, it’s often hard to stick to the 30% rule, with rents commonly taking up 40% or more of income. Conversely, in more affordable areas, you might be able to secure a larger or more comfortable living space for a fraction of that amount. Researching rent prices in your area can provide a realistic view of what’s manageable.

Lifestyle Choices and Habits

If you frequently dine out, enjoy hobbies, or travel often, these discretionary expenses will affect how much of your income can go toward rent. High lifestyle expenses might mean you need to look for cheaper housing to maintain a balance without sacrificing too much of what makes you happy.

Future Financial Goals

Think about your long-term goals. Are you saving for a house, planning to start a family, or building up retirement savings? If so, keeping rent as low as possible will help funnel more resources into these priorities. Alternatively, if you’re comfortable financially and want to enjoy a nicer space, you may decide to spend a bit more on rent, especially if it enhances your quality of life.

Evaluating these factors helps you set a realistic rent budget that aligns with your finances and goals, giving you peace of mind without feeling financially stretched.

Calculating How Much of Your Income Should Go to Rent

How much of your income should go to rent? The answer comes down to calculating what’s feasible based on your financial situation. Here’s a step-by-step approach to help you determine your ideal rent budget:

Step 1: Calculate Your Gross Monthly Income

First, determine your gross monthly income—this is the income before taxes. Let’s assume you earn $5,000 monthly.

Step 2: Use the 30% Rule or Another Budgeting Method

Using the 30% rule, you would calculate 30% of your gross monthly income ($5,000 x 0.3), which equals $1,500. Alternatively, you could try the 50/30/20 rule:

Essentials (50%): $5,000 x 0.5 = $2,500 (includes rent and other necessities)

Discretionary (30%): $5,000 x 0.3 = $1,500 (for lifestyle choices)

Savings and Debt (20%): $5,000 x 0.2 = $1,000

If you’re following the 50/30/20 rule and estimate other monthly essentials at $500, this would leave you with around $2,000 for rent.

Step 3: Adjust for Debt and Other Financial Commitments

Do you have significant debt payments each month? Adjust accordingly. If you’re paying $500 toward student loans, aim to reduce rent to 25% or less of your gross income to keep everything in balance.

Step 4: Account for All Housing-Related Costs

Your rent is just one piece of the puzzle. Consider utilities, internet, insurance, and possibly parking, and add these to your rent budget. For instance, if you anticipate $200 in additional costs, you might adjust your rent cap down to ensure you’re still within budget.

Step 5: Evaluate Based on Comfort

Ask yourself if the projected rent allows you to comfortably afford your other expenses and save for your goals. It’s fine to go slightly above or below a guideline if it fits your situation.

When to Break Away from Common Rent Rules

While the 30% rule and other budgeting guidelines can be useful, they don’t work for everyone. In some cases, breaking away from these rules may make sense:

Living in a High-Cost City

In cities like San Francisco, New York, or Boston, rent can eat up 40% or more of income. With limited affordable options, how much of your income should go to rent becomes a challenging question. The 30% rule often isn’t feasible, and it can make sense to spend more on rent if it means living in a safe and convenient area.

Low-Income Situations

For those with limited income, even 30% may not be enough to secure stable housing while covering other essentials. In such cases, allocating a higher portion to rent, though challenging, may be necessary.

Short-Term or Transitional Phases:

If you’re moving temporarily for work, school, or a specific opportunity, spending more on rent can offer flexibility and convenience. Higher rent costs are manageable when viewed as a short-term commitment rather than a long-term strain.

Investing in Career or Personal Growth

Sometimes paying more to live in a well-located area can boost career or personal opportunities. Proximity to job networks, reduced commuting time, or access to educational resources can make higher rent worthwhile for future benefits.

Breaking traditional rent rules is entirely reasonable when it aligns with a larger financial literacy or lifestyle strategy. Make sure you’ve thought about how much of your income should go to rent as part of a smart plan—so you can enjoy your home without stretching your budget too thin.

Tips for Reducing Rent Costs

If you’re finding rent to be a bit too much of a stretch on your budget, there are effective ways to save without compromising on comfort. Here are some practical strategies to help reduce rent costs:

Negotiate with Your Landlord

You’d be surprised at how open some landlords are to negotiating with dependable tenants. If you’ve built a good relationship and have been reliable with payments, you might be able to request a slight reduction in rent. Another approach is to ask if certain utilities—like water or internet—could be included in the rent, or if you could take on small maintenance tasks for a discount.

Find a Roommate

Sharing your space with a roommate can significantly cut down your rent. By splitting the cost, you could reduce your personal rent share to around 15-20% of your income, helping you comfortably afford a better space without maxing out your budget. Plus, sharing expenses like utilities can further stretch your dollar.

Consider Different Neighborhoods:

Moving just a few miles outside a city center or popular area can lead to substantial rent savings. Look for neighborhoods with good amenities, solid transit options, and lower average rent. You might find a great deal on a place that still offers a reasonable commute and enjoyable surroundings.

Look for Promotions and Move-In Deals

Many apartment complexes and landlords offer promotions to attract tenants, like a discounted first month’s rent, waived security deposits, or even a free month if you sign a longer lease. Keep an eye out for these deals, especially if you’re flexible with your move-in date—timing your search around these promotions can lead to serious savings.

Downsize to a Smaller Space

Often, we rent more space than we need. If you’re living alone or don’t need that extra bedroom, downsizing can save you hundreds each month. A smaller apartment also tends to be cheaper to heat, cool, and furnish, making it a double win.

Each of these tips offers immediate ways to cut down on rent costs, allowing you to put more toward savings, debt, or other goals. By exploring these options, you can manage your housing expenses while still enjoying a space that meets your needs.

Important Additional Expenses to Consider

When budgeting for rent, it’s easy to forget about the other costs that come with renting a home. Wondering how much of your income should go to rent? A good rule of thumb is to plan wisely to avoid overcommitting. Small expenses can pile up fast and strain your budget if you’re not prepared. Here are some key rental expenses to consider to avoid any unexpected financial surprises:

Utilities

Monthly utilities can include water, electricity, gas, internet, and even trash services. Some landlords bundle certain utilities in the rent, but many do not. If utilities aren’t covered, you could be looking at an extra $100–$300 per month, depending on the size of your apartment, location, and usage. Hot climates (air conditioning) or cold climates (heating) can push these costs even higher, so it’s smart to get an estimate before signing a lease.

Renter’s Insurance

Renter’s insurance is often mandatory and covers your belongings in case of theft, damage, or certain natural disasters. While it’s a relatively small cost, usually between $10 and $20 per month, it’s an essential one. For around $120–$240 annually, you get the peace of mind that your valuables are protected, which is especially important if you have expensive electronics, jewelry, or other personal items.

Application Fees and Security Deposits

Most landlords require an application fee, which can range from $25 to $100 per application and is generally non-refundable. Additionally, many leases require a security deposit, often equal to one month’s rent, which can be substantial in higher-rent areas. Be prepared to include this in your budget as a one-time, upfront cost when planning your move, as it can affect your overall affordability.

Parking Fees

If you live in a city, parking is another potential expense to keep in mind. Monthly parking fees in urban areas can range from $50 to several hundred dollars, depending on whether the parking is covered, secured, or in a prime location. For those who rely on a car, parking fees can be a significant cost that’s worth checking before committing to a property.

Repairs and Maintenance

Landlords cover major repairs, but minor fixes—like lightbulb replacements, basic cleaning supplies, or small upgrades—are usually the tenant’s responsibility. Plan for minor maintenance expenses so that you aren’t caught off guard by the little things that make a rental feel like home.

Taking extra expenses into account gives you a clearer picture of your total housing costs. It also helps answer the question, “how much of your income should go to rent?”—making it easier to budget and steer clear of surprises.

Smart Strategies for Saving on Rent

Saving on rent doesn’t mean you have to sacrifice comfort or quality. With some savvy strategies, you can reduce your monthly expenses and get the most out of your living situation. Here are several ways to help lower your rent burden:

1. Negotiate for a Long-Term Lease

If you’re planning to stay for a while, discuss a longer lease with your landlord. Many will offer a slight discount for commitments of 18 months or more since it provides them with tenant stability. It’s beneficial for both parties: you lock in a lower rate, and they secure consistent occupancy.

2. Rent in the Off-Season

Summer tends to be peak moving season, driving up rental prices. One of the best cost-saving strategies is to consider moving during the fall or winter months when demand is lower, and landlords are more willing to negotiate. You may find better deals simply by adjusting your move-in timing.

Look for All-Inclusive Rentals

Rentals that include utilities, internet, or parking can significantly lower your monthly expenses. By opting for a place with these costs covered, you not only save on utilities but also have the advantage of a fixed monthly budget with fewer surprise charges.

Use Referral Programs

Some rental communities offer incentives if you refer a friend. If someone you know is apartment-hunting, check with your landlord about referral discounts. This can sometimes reduce your monthly rent or provide a one-time credit.

Shop for Renter’s Insurance

Don’t settle for the first insurance policy you find. By comparing rates, you could save money each month. Some insurance providers offer discounts if you bundle policies, such as with auto insurance.

Do-It-Yourself Moving

Moving costs can add up quickly. Rather than hiring a moving company, consider renting a van and enlisting friends. This small choice can save you hundreds upfront and leave more in your pocket for other expenses.

With these strategies, you can manage your rent expenses more effectively, leaving room in your budget for other financial goals without compromising on quality or comfort.

Conclusion

How much of your income should go to rent? Ultimately, it depends on your income, lifestyle, location, and financial goals. While the 30% rule is a helpful starting point, your ideal rent budget should reflect your unique situation. Adjust your rent allocation based on your needs and priorities, and don’t hesitate to step outside standard rules when it aligns with your life goals.

From choosing the right budget method to considering all related costs, finding the right rent balance can give you the peace of mind to enjoy your space while building a secure future. By making an informed decision, you’re not just covering housing costs—you’re shaping a lifestyle that supports financial health and personal satisfaction.