There’s a weird thrill in the idea of holding a credit card for the first time. Not just because it feels grown-up, but because it’s a key that unlocks financial independence. How to build credit as a teenager isn’t just some adult chore you’re forced to figure out later in life. It’s a smart move you can start now, before the rent payments, student loans, or “adulting” really kick in.

And no, this isn’t about borrowing recklessly or chasing points. It’s about laying a quiet but powerful foundation. One where you’re trusted with more, because you’ve already proven you can handle it.

A good credit score doesn’t magically appear when you turn 25. It takes time. Which is exactly why starting as a teenager is such an advantage. You get a head start most people wish they had.

This guide isn’t full of boring finance lectures. It’s practical, real-world stuff. Steps you can actually take. Habits that will stick. And maybe a few things you’ll wish someone told you sooner.

So if you’re wondering where to start, or whether it’s too early… nope. You’re right on time. Let’s talk about how to build credit before the world expects you to have it all figured out.

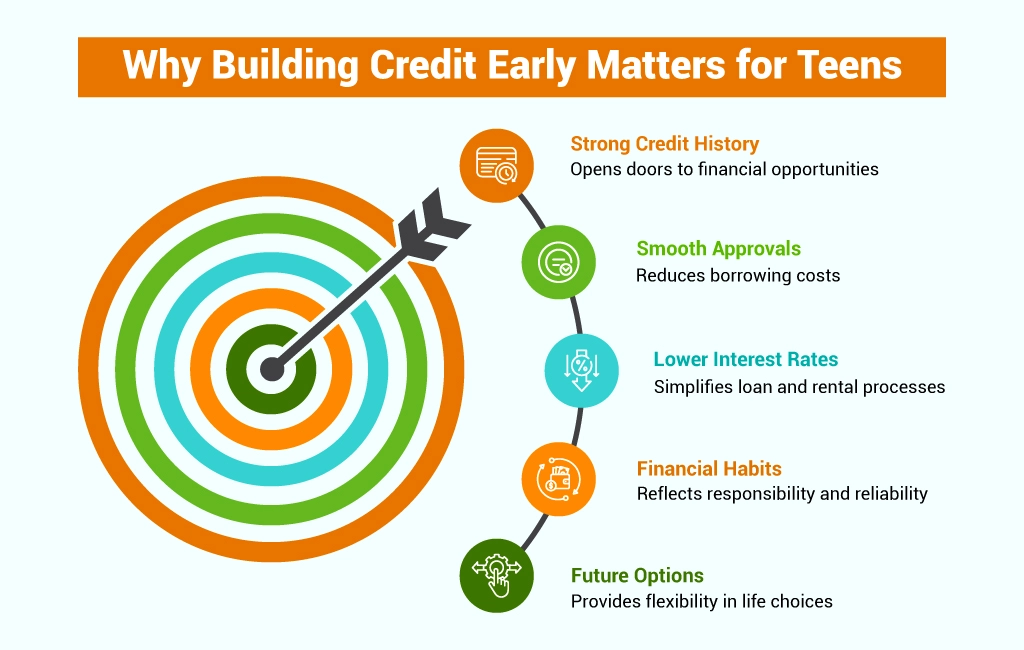

Why Building Credit Early Matters for Teens

Let’s be blunt, credit matters. A lot. And if you’re a teenager thinking, “Do I really need to worry about this now?” the answer is a resounding yes. Because building credit early isn’t just smart, it’s strategic.

A strong credit history opens doors. It can mean lower interest rates on student loans, smoother approvals for that first car, and fewer headaches when applying for an apartment. Lenders aren’t just looking at how much money you make, they’re looking at how you handle it. Payment history, credit utilization, the age of your accounts… they all paint a picture of your financial habits. Start building that picture at 16 or 17, and by your mid-twenties, you’re ahead of the game.

But here’s the thing: good credit isn’t only for borrowing money. It can influence everything from your cell phone plan to your car insurance premium. Some employers even check credit as part of the hiring process. Fair? Maybe not. Real? Absolutely.

Starting early gives you the gift of time. Credit takes years to mature, years you’ll lose if you wait until you “need” it. That first small step, a secured card, becoming an authorized user, sets things in motion.

The best part? You don’t need to be rich or a math genius to build good credit. You just need consistency, awareness, and a little head start. That’s it. Early credit building isn’t a buzzword, it’s your secret weapon. The sooner you begin, the more options you’ll have when it really counts.

So if you’re young and just starting out, don’t wait. Your future self will thank you, probably more than once.

Key Factors that Impact Your Credit Score

Your credit score isn’t some mysterious number floating in the financial clouds. It’s built from real actions, things you do (or don’t do) with your money. And the better you understand what drives it, the easier it becomes to build and protect.

The biggest factor? Payment history. This one’s simple: pay your bills on time, every time. Even one missed or late payment can ding your score and stick around for years. So whether it’s the minimum due on a credit card or a phone bill tied to your name, make it a habit: pay it before the due date, not on it.

Next up: credit utilization. This is how much of your available credit you’re using. Say you have a $10,000 credit limit. Using $9,000 of it? That’s a red flag. Ideally, keep your usage below 30%, and if you can manage under 10%, even better. It signals you’re responsible, not overextended.

Credit age also plays a role. The longer your accounts have been open, the better. That’s why becoming an authorized user on a parent’s older account can give your score a helpful boost early on.

Then there’s credit mix, having both revolving credit (like cards) and installment credit (like loans) shows you can juggle different responsibilities. And finally, new credit. Each time you apply for something, it triggers a “hard inquiry.” Too many in a short period makes you look risky.

Altogether, these “credit score factors” form the lens lenders use to judge your reliability. Understanding them puts the power in your hands. And the earlier you start working with them, not against them, the stronger your credit will be when it really counts.

Legal Age Requirements for Building Credit

Let’s take a quick detour into the fine print, because when it comes to credit, your age plays a bigger role than you might expect.

If you’re under 18, you can’t legally open your own credit card account. The law sees you as too young to take on that kind of financial responsibility. But that doesn’t mean you’re locked out of the credit world. One of the smartest moves at this stage is becoming an authorized user on someone else’s credit card, usually a parent or guardian.

Here’s how it works: you’re added to their account, and their credit behavior; on-time payments, low balances, can start appearing on your credit report. If they manage their credit well, it’s like getting a boost from a mentor. Just keep in mind that not all credit card issuers report authorized-user activity to the credit bureaus for minors, so it’s crucial to double-check the fine print.

Some issuers allow authorized users as young as 13. Others might set the minimum at 16. So yes, there’s a bit of variability based on the card and the issuer.

Once you turn 18, you can legally apply for a credit card in your own name. That’s when options like student credit cards and secured credit cards become available. However, if you’re under 21, federal regulations under the CARD Act require you to show proof of independent income, or have a co-signer. This rule was designed to prevent young adults from falling into unmanageable debt, but it also means you need to be prepared.

Bottom line: while you can’t dive into credit solo before 18, there are smart ways to start early. Use the rules to your advantage, and you’ll be ready to step into adulthood with a financial edge.

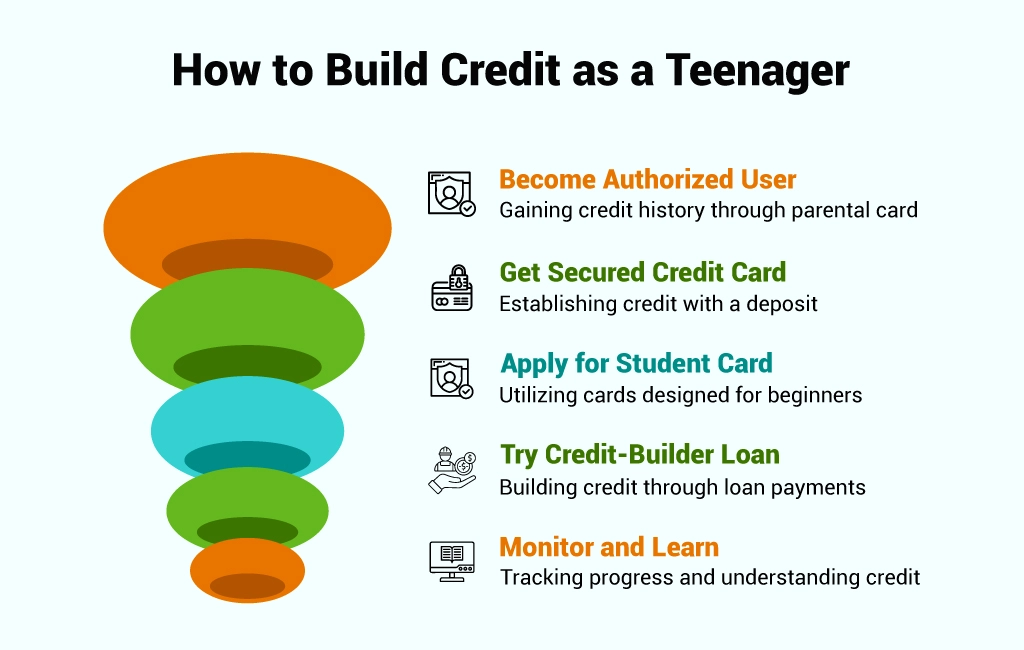

How to Build Credit as a Teenager: Step-by-Step Guide

Here’s where the rubber meets the road, where big financial dreams meet small, practical steps. If you’re serious about building credit as a teenager, there’s a method to the madness. And it’s not just one thing, it’s a combination of smart moves that work together over time. Let’s break it down.

1. Become an Authorized User (Even Before 18)

This is the easiest way to get your foot in the credit door. Ask a parent or guardian to add you as an authorized user on their credit card. If the account is in good standing, on-time payments, low balances, you’ll benefit from their history. But make sure the card issuer actually reports authorized user activity to the credit bureaus (not all do).

Also, have the awkward conversation: Will you have a card? What’s the spending limit? Who’s paying? It’s less about spending and more about history. Think of it as credit mentorship in action.

2. Get a Secured Credit Card (Once You’re 18)

If you’re legally an adult, a secured card is your training ground. You put down a deposit, say $10,000, and that becomes your credit limit. Use the card sparingly, never carry a balance, and pay on time. Many secured cards “graduate” into regular credit cards after a few months of responsible use, returning your deposit and unlocking higher limits.

3. Apply for a Student Credit Card (If You’re in College)

These cards are designed for beginners. They come with lower income requirements, modest credit limits, and sometimes perks like cashback on groceries or streaming subscriptions. Just remember: perks mean nothing if you carry a balance.

4. Try a Credit-Builder Loan

If credit cards aren’t your thing yet, this is a solid alternative. You “borrow” a small amount, often $5,000–$20,000, but the funds are held in a savings account. You make monthly payments, and those payments are reported to credit bureaus. At the end, you get the money and a better score.

5. Monitor and Learn

Use free apps like Credit Karma or Experian to track your progress. Watch how your habits affect your score. Learn from every statement, every balance, every bump in the road.

Building credit doesn’t happen overnight, but these steps, taken one by one, will get you there.

How to Check and Monitor Your Credit Report

You might be thinking, “I’m only 17, do I even have a credit report yet?” Fair question. And while you may not have a full credit profile or score just yet, your name might still appear in credit databases, especially if you’ve been added as an authorized user on someone else’s credit card. Or worse, if your identity has been stolen without you knowing. Yep, even teens can be victims of fraud.

That’s why it’s smart for parents to request a credit report on your behalf before you turn 18. All three major credit bureaus, Equifax, Experian, and TransUnion, allow this, though it takes a little paperwork.

Once you hit 18, you’re eligible to pull your own reports. Sites like Credit Karma, Experian, and CreditWise by Capital One let you track your score and monitor changes in real time, for free. But don’t just glance at your score. Dig into the details. Are there accounts you don’t recognize? Late payments you didn’t make? A suspicious inquiry from a bank you’ve never used?

Catching these things early can protect your credit before it even really starts. Monitoring your credit report isn’t just about curiosity, it’s about staying in control from the beginning.

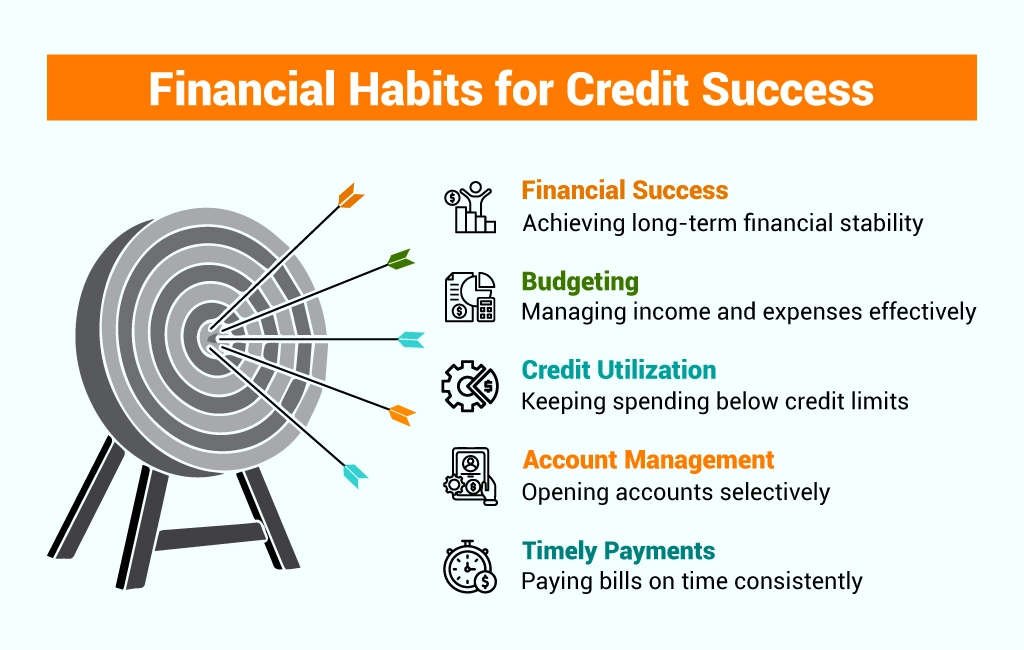

Essential Financial Habits for Credit Success

Building credit isn’t just about opening an account, it’s about how you manage it day in and day out. These habits might seem small, even boring. But they’re what separate those who struggle financially later from those who step into adulthood with real confidence.

First and foremost: pay your bills on time. Every time. That includes credit cards, yes, but also your phone bill, subscriptions, or any other recurring payments in your name. Late payments don’t just hurt your credit, they create a pattern that’s hard to break.

Keep your credit utilization low. If your card has a $10,000 limit, don’t spend $9,000 on it. Try to stay below 30% of your limit at any given time, lower is even better. High usage tells lenders you might be stretched too thin.

Avoid opening accounts just because you can. Every new application dings your score slightly. Too many at once? That’s a red flag. Be selective. Open accounts with purpose.

Budget wisely. Track what comes in, what goes out, and what can wait. It’s not flashy, but it’s freedom. Knowing where your money’s going gives you control, and control is the real flex.

Learn how interest works. Compound interest isn’t just a grown-up term; it’s a reality that affects your debt, savings, and investments. Understanding it early gives you power.

Financial literacy for teens isn’t optional anymore, it’s essential. Even something as simple as consistently paying your phone bill shows you’re ready. It’s all connected, and these habits form the backbone of lifelong financial success.

Common Credit Mistakes Teens Make and How to Avoid Them

Let’s talk about the missteps, because even smart teens fall into these traps. Building credit sounds simple on paper, but there are subtle mistakes that can quietly derail your progress. Here’s what to watch out for:

1. Believing Authorized User Status Is a Guaranteed Boost

Being added as an authorized user on a parent’s card can help, but it’s not automatic magic. Not all credit card companies report authorized-user data to the credit bureaus, especially if the user is under 18. And even if they do, some lenders discount that info when calculating your score. So it’s helpful, but not bulletproof. Know how your issuer handles it.

2. Maxing Out Credit Cards

It’s tempting. You finally have a card, so you test your limit, literally. But using too much of your available credit spikes your utilization ratio, which can tank your score fast. Aim to stay under 30%, or even better, under 10% of your limit.

3. Missing a Single Payment

One late payment might not seem like a big deal, but it is. It can stick to your credit report for up to seven years. Set calendar alerts, enable auto-pay, or use budgeting apps, whatever it takes to make sure bills don’t slip through the cracks.

4. Applying for Too Many Cards at Once

Chasing sign-up bonuses might sound fun until you realize that every application creates a “hard inquiry” on your credit. Too many of these in a short time makes you look risky. Spread out applications and only open what you need.

5. Ignoring Your Credit Report

Out of sight isn’t out of mind. Mistakes happen, accounts reported incorrectly, fraudulent charges, or activity that’s not even yours. If you’re not checking your reports, you won’t catch these in time to fix them.

Instead: Start with one safe, low-limit card. Use it for small purchases. Keep usage low. Pay in full. Monitor your credit. Build slowly. It’s not about doing it fast, it’s about doing it right.

Conclusion

So, there it is. How to build credit as a teenager laid out in practical, real-life steps. Not just theories, but actions you can take today. And while it may not feel urgent now, trust me, your future self will be incredibly grateful you started early.

Building credit as a teen isn’t about trying to game the system or rack up debt. It’s about learning how to manage money in a world that demands financial trust. It’s about showing lenders, landlords, and sometimes even employers that you can handle responsibility, and do it well.

Yes, there will be a learning curve. You’ll probably have to talk through things with your parents, maybe figure out what “APR” actually means, or remember your first payment deadline the hard way. But each small decision adds up. A single on-time payment might not seem like much, but a year’s worth? That tells a story. A good one.

Start simple: become an authorized user. Learn the ropes. Then, when you’re ready, step up to a secured or student card and keep your balance low, your payments punctual, and your mindset focused.

Remember—credit isn’t just a number. It’s a tool. And like any tool, it can build something great if used right… or cause a mess if mishandled. The good news? You’re already ahead of most by even thinking about this now.

Financial success doesn’t happen overnight. But starting your credit journey early gives you something many adults wish they had: a head start. By the time you’re applying for a car loan, your first apartment, or even your dream job, you won’t be starting from scratch—you’ll be walking in with a credit history that proves you’re ready.

So take that first step. Start building now. Because real confidence isn’t just about knowing your score—it’s knowing you’ve earned it.