When venturing into the world of homeownership, a fundamental question arises: “How does a mortgage work?” Understanding the mechanics of a mortgage is pivotal for anyone looking to own a home. This comprehensive guide is designed to break down and explain the concept of mortgages and answer some of your pressing questions.

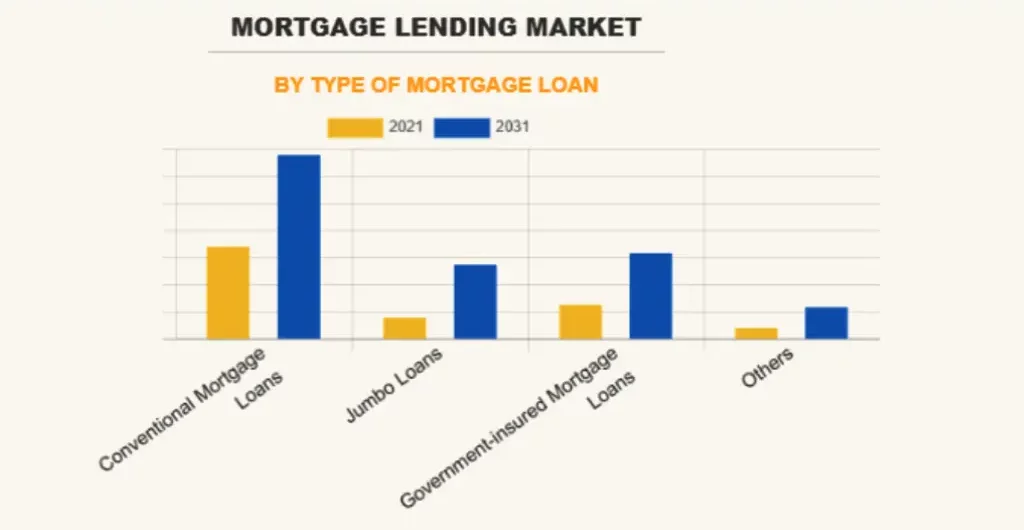

Image Courtesy: alliedmarketresearch.com

In 2021, the worldwide mortgage lending sector was valued at $11,487.23 billion. By 2031, it’s estimated to increase to $27,509.24 billion, with an anticipated CAGR of 9.5% from 2022 to 2031.

Understanding Mortgages

A mortgage is a type of loan tailored specifically for real estate. In this context, the borrower agrees to borrow money from a lender (often a bank or mortgage company) to buy a home or refinance an existing mortgage.

Mortgages represent a cornerstone of the real estate industry, yet the intricacies remain in mystery for many. Basically, how does a mortgage work? A mortgage is a form of loan specifically designed for acquiring or refinancing real estate property. When you take out a mortgage, you are entering an agreement with a lender (typically a bank or a mortgage company) that they will lend you the funds needed for the property, and in return, you will pay back the borrowed amount, with interest, over a predefined period.

The terms of a mortgage can vary widely based on several factors. These can include the type of mortgage selected (such as fixed-rate or adjustable-rate), the duration of the loan, interest rates, and the borrower’s creditworthiness. As the borrower, you are bound to make regular payments, which will be applied to the principal amount borrowed and the accrued interest. Over time, a larger percentage of these monthly payments goes towards reducing the principal amount while the interest portion decreases.

Understanding how a mortgage works is the first step toward owning a property for many potential homeowners. It’s a commitment that lasts several years, even decades, so knowing how they function is crucial. Getting familiar with mortgage terms, navigating interest rates, and understanding your responsibilities as a borrower can make the homeownership journey smoother and more manageable.

How Does a Mortgage Work?

Embarking on the journey of homeownership is an exciting milestone. Yet, many find themselves grappling with the complexities of mortgages. After all, purchasing a home is one of the most significant financial decisions most of us will make in our lifetimes. At its essence, a mortgage is a long-term loan provided by a lender to a borrower, with the property in question serving as collateral. Payments are made over time, covering several components such as the loaned amount, interest, and additional charges. This guide aims to break down the four primary elements of a mortgage: Principal, Interest, Taxes, and Insurance.

Principal

The principal is the initial amount borrowed to purchase the home. It represents the property’s sale price minus any down payment made by the borrower. Over time, with each mortgage payment, a portion is dedicated to reducing this principal amount, bringing you one step closer to fully owning the property.

Interest

Interest is the cost of borrowing money and how lenders profit. It’s expressed as a percentage of the principal. In the early stages of a mortgage, a higher proportion of your monthly payments goes towards paying off this interest, which gradually shifts more towards the principal as time progresses.

Taxes

Property taxes are a crucial part of homeownership. Levied by local governments, these taxes fund essential services such as schools, roads, and emergency services. Many mortgage providers will include these taxes in your monthly payments, collecting and holding them in an escrow account, ensuring they are paid on time.

Insurance

Home insurance protects homeowners against potential damages to the property. Most lenders will require borrowers to maintain adequate insurance coverage for the property’s lifespan under the mortgage. Like taxes, this insurance fee can be integrated into your monthly mortgage payments, offering peace of mind and financial protection.

What is the Process of Mortgage

After understanding how a mortgage works, Navigating the world of mortgages can initially seem daunting However, by understanding each step in the process, prospective homeowners can approach this journey with confidence and clarity. Below, we outline the typical stages of securing a mortgage.

1. Get Your Pre-Approval

Getting a mortgage pre-approval is prudent before diving deep into the housing market. This step estimates how much a lender will offer based on a preliminary review of your financial history. Not only does this give you a clear budget framework, but it also makes you a more attractive buyer in the eyes of sellers.

2. Find a Property

Armed with your pre-approval, you can begin the exciting house-hunting phase. Whether you’re doing this independently or with the aid of a real estate agent, it’s essential to find a property that aligns with both your budget and personal needs.

3. Apply for a Mortgage

Once you’ve identified your dream property, the next step is formally applying for a mortgage. This involves providing the lender with detailed information about the property and further documentation regarding your financial status.

4. Complete Loan Processing

After submitting your application, the lender will begin processing your loan. This entails thoroughly reviewing all provided documents, including property valuations and verification of your financial credentials.

5. Go Through the Underwriting Process

The underwriting phase is pivotal. Here, an underwriter assesses all the information to determine your lending risk. They’ll validate your financial standing, ensure the property is worth the purchase price, and confirm that all lending criteria are met.

6. Close on the Property

Upon successful underwriting, you’ll arrive at the closing stage. This involves signing all the necessary paperwork, finalizing the loan terms, and initiating funds transfer. Once completed, the keys to your new home will be in your hands, marking the conclusion of the mortgage process.

Different Types of Mortgages and How They Work

The world of home financing offers a plethora of mortgage options, each tailored to meet specific financial circumstances and goals. Choosing the right mortgage type can greatly influence the cost of your home over time.

Fixed-rate mortgage

A fixed-rate mortgage is the epitome of stability in the home financing realm. With this mortgage type, the interest rate remains constant throughout the loan term, ensuring that monthly payments stay unchanged.

This consistent payment structure is ideal for borrowers who prioritize budgeting predictability and those who intend to stay in their homes long-term. Locking in a fixed rate can be particularly advantageous in periods of low-interest rates.

Adjustable-rate mortgage (ARM)

In contrast to its fixed-rate counterpart, an adjustable-rate mortgage (ARM) has an interest rate that can change periodically. Typically, ARMs start with a lower initial interest rate, which adjusts based on a specific index after a predetermined period.

The allure of ARMs lies in the potential for lower initial payments. However, borrowers must be prepared for fluctuating monthly payments, which can increase if interest rates rise. It’s vital to understand the adjustment frequency and rate caps before committing.

Long-term loans

Often spanning 30 years, long-term loans are a popular choice among homebuyers. These loans offer smaller monthly payments spread over an extended period, making them more manageable for many.

While the long tenure reduces monthly financial strain, it’s worth noting that borrowers tend to pay more in interest over the loan life compared to shorter-term options.

Short-term loans

Short-term loans, such as 10 or 15-year mortgages, are designed for those looking to pay off their homes faster. The monthly payments are higher, but the trade-off is significant interest savings over the loan’s life.

Ideal for those with stable financial situations, short-term loans can lead to quicker equity buildup and the satisfaction of owning a home outright in less time.

FHA loans

Federal Housing Administration (FHA) loans cater to borrowers with lower credit scores or minimal down payments. These government-backed loans provide lenders with added security, often leading to more lenient qualification criteria.

While the low down payment is attractive, it’s essential to factor in the mandatory mortgage insurance, which can add to the loan’s overall cost.

Conventional loans

Any government entity does not back conventional loans. They typically require a higher credit score and larger down payment than FHA loans, but they come without the necessity of upfront mortgage insurance.

These loans often come with competitive interest rates, especially for borrowers with excellent credit. They can be either fixed-rate or adjustable-rate, offering flexibility in terms.

VA loans

A boon for eligible veterans and service members, VA loans are backed by the U.S. Department of Veterans Affairs. These loans often require no down payment and have competitive interest rates.

Aside from the financial benefits, VA loans boast lenient qualification standards, making homeownership more accessible to those who’ve served their country.

USDA loans

The U.S. Department of Agriculture backs USDA loans to promote homeownership in rural and select suburban areas. These loans often come with zero down payment and have favorable interest rates.

Eligibility is based on location and income levels, so checking whether the property and borrower meet the USDA’s criteria is crucial.

Key Mortgage Terms to Know

The mortgage landscape, while exciting, is punctuated with terms and jargon that can often be confusing for both first-time and seasoned homebuyers. Understanding these terms is not just beneficial—it’s crucial to making informed decisions. In this article, we unravel some of the most fundamental mortgage terms you will likely encounter on your homeownership journey.

Promissory Note

A promissory note is a written agreement where the borrower commits to repaying a specific amount of money to the lender within a set timeframe. This document details the loan’s interest rate, repayment terms, and the consequences of defaulting. In essence, the borrower promises to pay back the loan.

Mortgage

While often used interchangeably with “home loan,” a mortgage is technically the legal instrument that secures the loan against the property. It provides the lender the right to take possession of the property through foreclosure if the borrower fails to meet their loan obligations.

Deed of Trust

Similar to a mortgage, a Deed of Trust involves three parties: the borrower, the lender, and a trustee. This document allows the trustee to hold the property title on behalf of the lender. Should the borrower default, the trustee has the authority to sell the property to recover the lender’s funds.

Mortgage Closing Costs

Mortgage closing costs encompass the various fees and expenses incurred during the mortgage transaction process. These can include origination fees, title search fees, appraisal costs, and more. Typically, closing costs range between 2% to 5% of the home’s purchase price.

Discount Points

Discount points are a form of prepaid interest that a borrower can purchase to lower their mortgage’s interest rate. One discount point typically costs 1% of the total loan amount and can reduce the interest rate by a fraction, usually 0.25%. Buying points benefit those planning to stay in their homes for a long time.

Note Rate

The note rate, often simply called the “mortgage rate,” is the interest rate stated on the promissory note. It determines the interest portion of your monthly mortgage payment. This rate does not consider other costs, such as insurance or fees, associated with the loan.

Annual Percentage Rate (APR)

While the note rate gives you the basic interest rate, the APR provides a broader view. It represents the total cost of borrowing annually, encompassing the interest rate, fees, and other charges. Comparing APRs from different lenders can offer a clearer perspective on which loan might be more cost-effective.

Mortgage Insurance

Mortgage insurance is a coverage plan that safeguards lenders from financial setbacks stemming from homeowners failing to meet their loan obligations. Typically required for borrowers who can’t make a 20% down payment, it’s either added to your monthly mortgage payment or charged as an upfront fee, depending on the loan type.

Why Do Home Buyers Use Mortgages?

Most individuals need the means to pay for a home outright. Mortgages provide the leverage to acquire property and repay the amount over a fixed period.

Homeownership is a shared vision for many, and mortgages have emerged as the primary tool to make this dream a reality. But why do most homebuyers opt for mortgages instead of saving up to buy a house outright? The reasons are manifold and deeply rooted in both practicality and long-term financial strategy.

For starters, real estate, especially in prime areas, is expensive. The time it would take for the average person to save enough money to buy a house outright is significant. For many, property prices would have escalated by the time they’ve saved enough, driven by inflation and other economic factors. Mortgages allow individuals to buy a home now and lock in its current price. This provides immediate access to the benefits of homeownership and potentially allows them to benefit from property appreciation over time.

mortgages can also play a strategic role in wealth management and financial planning. With historically low-interest rates, a mortgage can be considered “cheap money.” Buyers can keep their liquid assets invested elsewhere by financing a home with a mortgage, potentially earning a return higher than their mortgage interest rate. This strategy can optimize wealth growth. Furthermore, the potential tax benefits of mortgage interest can make financing even more attractive. In light of our detailed discussion of how a mortgage works, a mortgage is more than an essential; it is a wise investment.

Benefits of Mortgage Loan

Navigating the path to homeownership can be both thrilling and daunting. While the financial commitment is significant, the benefits of obtaining a mortgage loan often extend beyond the surface-level advantages of owning property. Mortgages can, directly and indirectly, bring about positive changes in an individual’s financial landscape.

It Boosts Your Credit Score

One of the cornerstones of a solid financial profile is a good credit score. Consistent and timely mortgage payments can significantly enhance this score. How? Credit rating agencies often view mortgages as ‘good debt’—a testament to an individual’s ability to manage long-term financial obligations. As you meet your mortgage payment deadlines, you not only inch closer to outright homeownership but also cultivate a robust credit profile, which can benefit future financial endeavors.

You Might See Some Tax Benefit

The tax implications of homeownership are often favorable. In many jurisdictions, the interest paid on a mortgage, especially in the loan’s early years when interest constitutes a larger portion of the monthly payment, can be tax-deductible. This effectively reduces the net cost of the loan. Additionally, certain property-related taxes also offer deductions, ensuring that homeownership, when paired with astute tax planning, can be more affordable than initially perceived.

You Could Put the Extra Funds to Work Elsewhere

Opting for a mortgage does not just facilitate property purchase; it also allows for liquidity. Imagine having to save up the full price of a house in cash. It could take years, even decades. By financing a significant portion of the property value, you retain a good chunk of your savings, which can be invested elsewhere. This liquidity ensures that you can capitalize on other financial opportunities, be it stock market investments, business ventures, or even further education. In periods of low-interest rates, this strategy can yield returns that outpace the mortgage cost, leading to optimized wealth growth.

You Gain Leverage in Building Equity

Leverage is a powerful financial concept, especially in real estate. With a mortgage, you can control a large asset (your home) with a relatively small amount of your own money (the down payment). Over time, as the value of your home appreciates, you’re not just earning on the equity you’ve paid into the house but on its entire value. This means you could see a higher return on investment than if you bought the property outright.

A Hedge Against Inflation

Mortgages, especially fixed-rate ones, offer an intrinsic advantage in an inflationary environment. As inflation rises, the real value of money decreases. However, with a fixed-rate mortgage, your monthly payments remain unchanged throughout the loan term. This means, in effect, you’re paying back your loan with “cheaper” money as time progresses. If property values rise with or faster than inflation, you’re doubly protected: your home’s value increases while your payment stays the same, making homeownership a savvy long-term financial strategy.

How to Qualify for a Mortgage

Embarking on the journey to homeownership often starts with understanding how to qualify for a mortgage. Mortgage lenders look at various factors to determine an applicant’s eligibility and the terms they might extend a loan.

Your Credit Score

A credit score is a numerical representation of your creditworthiness, influenced by your credit history, outstanding debts, payment behaviors, and more. Lenders use this score to gauge the risk associated with lending to you. A higher credit score can lead to more favorable loan terms, including lower interest rates. If your score isn’t where you’d like it to be, consider improving it before applying for a mortgage.

Your Debt-to-income Ratio

This metric contrasts your monthly financial obligations with your pre-tax monthly earnings. Financial institutions utilize it to determine your ability to handle monthly financial commitments and repay funds. A reduced debt-to-income proportion suggests a favorable balance between liabilities and earnings, marking you as a more appealing candidate to creditors.

Your Down Payment

The down payment represents your initial investment in the property. While some loan types require minimal down payments, a larger down payment can work in your favor. It can reduce your loan amount, earn better interest rates, and sometimes help you avoid additional costs like private mortgage insurance.

Your Rainy-day Reserves

Lenders often want to see that you have some savings for emergencies. This reserve assures them that even if they face financial hiccups in the future, like job loss or medical emergencies, they’ll still be able to make their mortgage payments.

Your Property Type

The type of property you’re looking to buy can influence mortgage terms and interest rates. For instance, interest rates for multi-family homes might differ from those for single-family homes. Similarly, a loan for a primary residence might have different requirements than one for an investment property or vacation home.

Your Occupancy Plans

How you intend to use the property—whether as a primary residence, a vacation home, or an investment property—can affect your mortgage rates and requirements. Typically, primary residences qualify for lower interest rates because lenders assume homeowners will prioritize their residence’s mortgage payments over other properties.

Pros and Cons of a Mortgage

A mortgage is a substantial financial commitment, often spanning decades of a borrower’s life. Like any major decision, obtaining a mortgage comes with its set of advantages and disadvantages. By understanding both the pros and cons, potential homeowners can make informed decisions that best align with their financial goals and lifestyle aspirations.

Pros of a Mortgage

You’ll achieve homeownership: One of the most significant advantages of a mortgage is that it enables individuals to achieve homeownership without waiting years or even decades to save up the entire purchase price of a home. This means you can enjoy the benefits of having your own place, such as stability, freedom, and personalization, much sooner.

You can cash in your equity: As you make mortgage payments and the value of your home appreciates over time, you build equity. This equity can be tapped into later by selling the property for a profit or through a home equity loan, providing financial flexibility for other endeavors or needs.

Your credit score may improve: Consistently making timely mortgage payments can boost your credit score. Since a mortgage is often a borrower’s largest debt, and houses are generally considered stable investments, responsible handling of mortgage payments reflects positively on one’s credit history.

You may have extra tax benefits: In many jurisdictions, the interest paid on a mortgage and related expenses can be tax-deductible, reducing your annual tax liability. This effectively reduces the loan’s net cost, making homeownership more economically viable.

Cons of a Mortgage

You risk losing your home: The most significant risk of taking on a mortgage is the possibility of foreclosure. If you fail to keep up with your mortgage payments, the lender has the right to take ownership of the property through a legal process, leaving you without the home you’ve invested in.

Your home’s value could drop: Real estate markets can be volatile. There’s a risk that the value of your home could decrease over time. If this happens, you might find yourself in a situation where you owe more on your mortgage than your home is currently worth, leading to potential financial strain.

Final Words

So, how does a mortgage work? It’s a structured way of purchasing a home through borrowed funds, repaid over time. For many, a mortgage is the key to homeownership, but understanding its mechanics is pivotal. Make informed decisions, consider the pros and cons, and ensure a smooth path to your dream home.

Obstacles to securing a mortgage include a poor credit history, a high debt-to-income ratio, unstable employment, insufficient income or down payment, and potential property appraisal or structure issues.

Mortgages typically come in terms like 15 or 30 years. Lenders usually prefer applicants with at least two years of consistent employment and a few years of credit history. Still, the specifics can vary based on the loan type and individual financial circumstances.

The initial step in obtaining a mortgage is assessing your financial health, which includes checking your credit score and understanding your debts and savings, followed by seeking pre-approval from a lender or mortgage broker.

Benjamin Jones has a bright and cheerful personality. He had many certifications including: CPA, CFA®, CFP®, and an MBA from the University of Chicago.

He worked for Ernst & Young LLP and is one of the youngest instructors at Becker, he was ranked in the top 5 nationally (out of more than 600). At EduCounting, Benjamin Jones provides videos, podcasts, blogs, and much more. When he isn't teaching or creating he enjoys biking, spending time with his family, and learning even more.