Think of investing like picking the right tools for a garden, you’re not just tossing seeds and hoping for the best. You’re choosing from different types of investment, each with its own potential to grow your wealth or protect it when markets get stormy. Whether you’re aiming for steady, long-term growth or looking for a buffer against life’s financial curveballs, understanding where and how to invest is key.

From stocks and bonds to real estate and ETFs, we’ll walk through the full range of investment options, safe to bold, local to global, so you can make confident, informed choices without the jargon overload.

What is Investment?

Investment is simply putting your money, or sometimes your time, into something with the expectation it will grow in value or generate income over time. That “something” can be anything from stocks and bonds to property or mutual funds. Each offers different ways to earn dividends, interest, rental income, or a rise in market value.

The goal? It depends. You might want to outpace inflation, build long-term wealth, or just avoid letting your cash sit idle. We’ll break them down so you know what fits your goals, and more importantly, what doesn’t.

Main Categories of Investment

Let’s pause here for a quick comparison mini-table; this might feel too tidy, but hey, tables help keep things clear:

| Investment Type | Common Regions | Typical Investor Profile | Risk/Return Expectation |

|---|---|---|---|

|

Equity (Stocks) |

Equity (Stocks) |

Growth‑oriented, patient |

High risk, high return |

|

Fixed‑Income (Bonds) |

Developed & emerging |

Income‑seekers, conservative |

Low–medium risk, steady return |

|

Cash Equivalents |

Everywhere |

Ultra‑conservative savers |

Very low risk, low return |

|

Real Estate |

Locally/global |

Long‑term, hands‑on |

Medium risk, mixed return |

|

ETFs |

Global |

Beginners to pros, diversifiers |

Varies by ETF type |

|

Commodities |

Global commodities hubs |

Inflation hedgers, speculators |

High risk, volatile returns |

|

Hybrid Investments |

Various |

Balanced portfolios |

Medium risk, blended returns |

|

Alternative Investments |

Global, niche |

Accredited or adventurous |

High risk, potentially high return |

That’s our rough forms of investment map, maybe not perfect, but you get the drift.

Equity Investments (Stocks)

Here’s where you’re buying a slice, becoming a shareholder. Historically, markets like the S&P 500 have returned about 10% annually over time. Pretty sweet, but don’t ignore that volatility, some years are rough, wiping you out. Stocks are for when you’re aiming for growth and can tolerate the jolts.

Fixed‑Income Investments (Bonds)

Buying a bond means lending to an issuer, governments or corporations, and getting interest plus principal eventually. Corporate bonds offer steady income and are considered less volatile than stocks, though they’re not foolproof. Government bonds? Safer still, though returns are typically lower.

Cash & Cash Equivalents

Think high-yield savings accounts, money market funds, and CDs. They’re safe, and ready-to-go liquid, but returns are modest, and inflation can gobble up those gains.

Real Estate Investments

Physical property, real estate investment trusts (REITs), rental income, real estate can anchor a portfolio. It’s less liquid and more of a hands-on gig, but for many, the steady rent checks (and potential appreciation) are comforting. REITs offer liquidity and ease of access via exchanges.

Exchange‑Traded Funds (ETFs)

ETFs are like baskets, holdings inside might include stocks, bonds, commodities, say, but you buy (and sell) one share on an exchange. Super handy for instant diversification. Low cost, transparent, and flexible, great for beginning investors, especially those who’d rather not pick single stocks.

Commodities

Here you’re investing in stuff, gold, oil, agricultural goods, maybe via futures contracts or commodity-based ETFs. Firecracker volatile, yes, but sometimes a great inflation hedge or portfolio stabilizer. Bank of America notes that a 60% stock/40% commodities mix has historically beaten a 60/40 stock/bond portfolio by 0.8 percentage points annually since 1945, though that’s no guarantee for tomorrow.

Hybrid Investments

These mix elements of equities, fixed income, maybe real estate, balancing growth and stability. Think balanced mutual funds or target-date funds, often used for retirement.

Alternative Investments

Catch‑all for the non‑traditional: real assets, hedge funds, private equity, collectibles, cryptocurrencies, even art or wine. They can offer unique returns, and diversification, but often come with complexity, fees, and sometimes high minimums or illiquidity.

Risk Levels in Different Types of Investments

Let’s talk about something every investor wrestles with: risk. It’s unavoidable, but it’s also not the enemy, it just needs to be understood and managed.

Broadly, we can break investments into three risk categories:

Low risk includes cash equivalents like high-yield savings accounts, certificates of deposit (CDs), and government bonds. These are the “steady Eddie” choices. They don’t earn much, but they’re predictable, and for people looking to preserve capital, they’re hard to beat.

Medium risk covers things like corporate bonds, real estate, and many hybrid or balanced funds. These offer a mix of safety and growth potential. You might earn more than you would from a savings account, but there’s still a chance, albeit smaller, of losing value.

High risk investments include stocks, commodities, and alternative assets like cryptocurrencies or venture capital. These can swing wildly. One month you’re up 20%, the next, you’re down just as much. That volatility can be stressful, but the long-term returns often justify the ride, if you’ve got the stomach for it.

Now, about the risk-return trade-off: generally, the more risk you take on, the higher your potential return. But it’s not perfectly linear. Real estate might offer stable returns with medium risk, while commodities can be all over the place.

Ultimately, your comfort level matters just as much as the math. The key is finding a mix that fits both your goals and your gut. Risk isn’t bad, it just needs to be the right kind of risk for you.

Time Horizon and Investment Goals

Let’s take a moment to talk about time. Specifically, how long you’re planning to keep your money invested, what’s called your time horizon. It might not sound thrilling, but it’s a big deal. Why? Because the type of investment that’s right for you often depends more on timing than anything else.

Short-term goals, we’re talking less than three years, usually call for safer bets. Think high-yield savings accounts, money market funds, or short-term government bonds. The goal here isn’t to make a fortune. It’s to keep your money intact and easily accessible when you need it.

Medium-term goals, say 3 to 10 years out, give you a bit more flexibility. You might consider a balanced mix: perhaps some bonds, diversified ETFs, and even a little real estate. There’s time to recover from minor market dips, but not enough to absorb major losses without feeling the sting.

Long-term goals, over a decade away, open the door to higher-risk, higher-reward investments. Equities (stocks) often shine here, and real estate or even some alternative assets can play a role. You’ve got the luxury of time to ride out market swings.

At the end of the day, matching your investments to your timeline is half the strategy. It’s not just about picking what’s “hot” or what earned 12% last year. It’s about choosing what aligns with your goals, comfort level, and when you actually need that money. Timing really is everything.

Best Investments for Beginners

Starting out in investing can feel a bit like walking into a gym for the first time, not quite sure where to begin, but knowing you probably should be doing something. The good news? You don’t need to go full Wall Street right away. A few simple, beginner-friendly options can help you ease in without the overwhelm.

For starters, high-yield savings accounts or money market funds are great places to park your cash while earning a little interest. They’re ultra-low risk and keep your money within reach, perfect if you’re still figuring things out.

Next, consider ETFs, especially broad-market ones like an S&P 500 ETF. These give you instant diversification across hundreds of companies with just one purchase. They’re low-cost, easy to buy, and don’t require you to be an expert in picking stocks.

If you’d prefer a more hands-off approach, a robo-advisor might be ideal. These automated platforms build and manage a portfolio for you based on your goals and risk tolerance.

The key is to start small and stay consistent. These investment options are simple, relatively safe, and a great way to build confidence, without getting buried in jargon or sky-high fees.

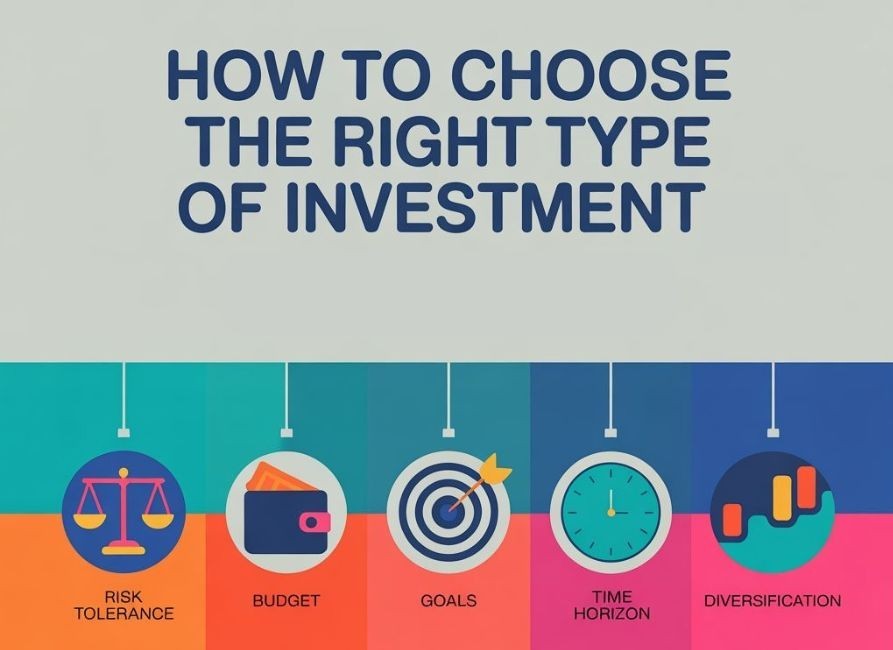

How to Choose the Right Type of Investment

Not sure where to start? Totally normal. Here’s a quick checklist to help narrow it down—no jargon, no fluff:

1. Risk Tolerance

How much can you realistically handle losing, financially and emotionally?

Some people can stomach big swings. Others lose sleep over a 5% dip. Be honest with yourself. Your comfort zone matters more than a headline return.

2. Budget

How much do you have to invest?

Are you starting with $100, $10,000, or somewhere in between? Some investments let you start small, others don’t. Know what you’re working with.

3. Goals

What are you aiming for?

Growth over the long term? Steady income now? Safety and preservation? Maybe a mix? Your answer shapes the type of investment that fits, stocks, bonds, real estate, or even just high-yield savings.

4. Time Horizon

How long can you leave your money untouched?

If you need it in a year, you’ll invest very differently than if you won’t touch it for 15. Time affects risk, and reward.

5. Diversification

Are you spreading your risk?

One investment is rarely enough. Spread across types, sectors, and maybe even countries. It’s a simple way to protect yourself from the unexpected.

How to Start Investing

Here’s a casual but practical step-by-step plan:

1. Build an emergency fund: 3–6 months of expenses in something liquid.

2. Pay off high‑interest debt: those rates tend to outpace what investments return.

3. Decide how hands-on you want to be:

a. Try a robo-advisor: quick, diversified, mostly set-and-forget.

b. Or use a brokerage account to DIY, start small with ETFs or fractional shares Investopedia.

4. Pick your mix: maybe a bit in cash equivalents, a chunk in ETFs (stocks, bonds), and later, explore real estate or alternatives.

5. Stay consistent: Invest monthly, not just all at once, dollar-cost averaging helps smooth out volatility.

6. Keep learning: Read, follow financial news, maybe check resources like the SEC, OECD, or World Bank for stats and guidance.

Wrapping Up

What’s the headline here? There are many types of investment, stocks, bonds, ETFs, real estate, commodities, hybrids, and alternatives, and each brings its own flavor of risk, return, and suitability depending on your goals and timing. Beginners might do well with ETFs and cash equivalents while building up, more adventurous investors can venture into real estate or alternatives once they’re comfortable. Balance, diversification, and clarity about your purpose will keep you more grounded than chasing the shiniest new thing.

Maybe your next step is exploring robo‑advisor platforms, or reading EC’s ETF or beginner investing resources. Regardless of where you start, knowing these investment options and how they fit your individual story is already a huge win. And hey, if you want help picking a starting ETF or drafting your mix, just say the word.

Remember, it’s not about perfection, it’s about staying real, setting modest steps, and learning as you go. You’ve got this, and maybe, just maybe, that dinner table brag about your first portfolio won’t be so hypothetical after all.