Acquiring a home is a fulfilling aspiration for numerous individuals, but it can be difficult to accomplish when facing substantial debt. Debt consolidation is often considered a potential solution for people wanting to buy a home, but you need to be aware of how it could impact your plans.

Debt consolidation is when you merge multiple debts into a bigger loan with a lower interest rate. It can help you save money by reducing the interest you pay each month and making it easier to manage multiple loan payments. The situation may positively or negatively impact your credit score.

When considering financial management, one question often arises: “Does debt consolidation affect buying a home?” Navigating the landscape of personal finances can be complex, particularly when large investments like home buying are in your plans. This article sheds light on how debt consolidation could impact your ability to purchase a home and the various aspects that must be considered.

Understanding Debt Consolidation

Debt consolidation is when you combine multiple sources of debt into one loan. It can help make managing finances easier and save money on interest payments.

Often, this process can simplify your financial management, lower your monthly payments, and possibly reduce interest rates. However, it’s essential to understand that consolidating your debt doesn’t erase it—it simply restructures it to make it more manageable.

The process of consolidation may affect your credit score. While a temporary dip may occur during the initial stages, properly managing your consolidated debt can improve your credit standing over time, providing you maintain regular payments.

It’s also important to note that debt consolidation isn’t ideal for everyone. The best way to determine if it’s the right choice is to consider your long-term financial goals and develop an action plan with a financial advisor or credit counselor.

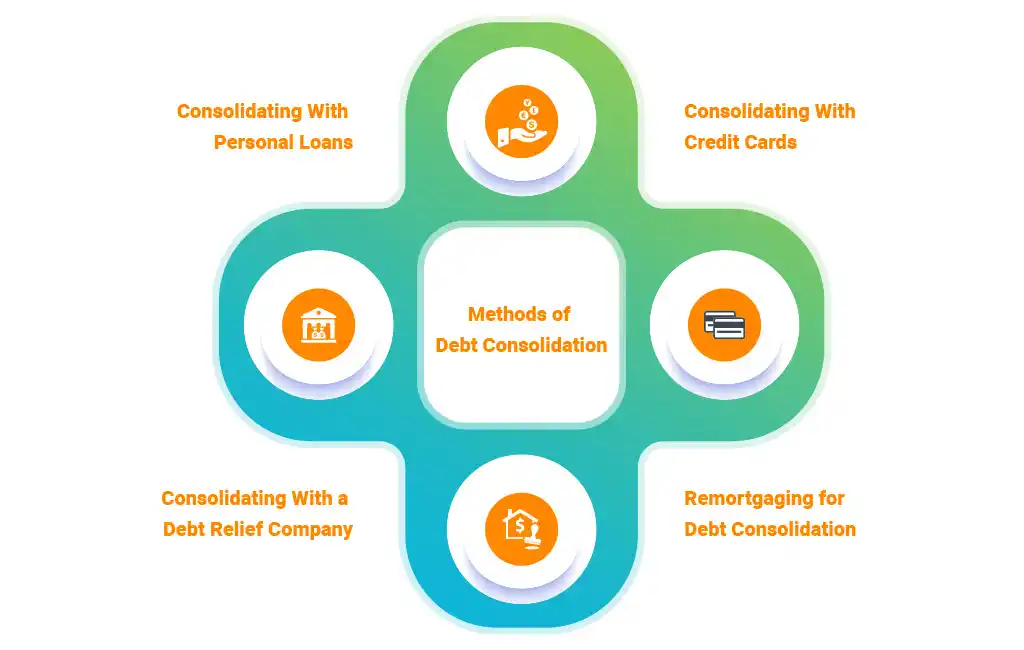

Different Methods of Debt Consolidation

A variety of methods can be employed to consolidate debt, each having a unique impact on your finances. When considering how debt consolidation affects buying a home, it’s important to understand the options available. So, let’s take a closer look at the most common ones: consolidating with personal loans, credit cards, and debt relief companies.

Consolidating With Personal Loans

Imagine this: Instead of tracking multiple payments and juggling various interest rates, you only have to remember one monthly payment. That’s the goal of consolidating with personal loans. You can take out a loan from a bank or other financial institution and use it to pay off multiple debts.

Personal loans can be a great way to consolidate your debt. They bundle all your existing debts—credit cards, medical bills, maybe even student loans—into one tidy package. So, if you’re organized and have a solid repayment plan, this can be a great way to manage your debt.

Consolidating With Credit Cards

Another method you might consider is using a balance transfer credit card to consolidate your debts. This is like playing musical chairs with your debt—moving it all onto one credit card, often with a lower or even zero interest rate for a promotional period.

If you can pay off the balance before the promotional period ends, this approach could be a good option. But be careful—once that period is over, the interest rate could jump up higher than your original cards. And don’t forget to account for any balance transfer fees. You’ve got to read the fine print, my friend.

Consolidating With a Debt Relief Company

If the thought of dealing with your debt is overwhelming, and you can’t see a clear path out, a debt relief company might be the way to go. It sounds great, right?

But remember, there’s no free lunch. These companies often charge fees, which could negatively impact your credit score. Plus, your creditors aren’t required to negotiate with these companies. So, if you choose this path, do your homework and understand the potential downsides.

Remortgaging for Debt Consolidation

One final option for consolidating your debt is to remortgage. This involves taking out a new loan against your home’s equity and using the money to pay off existing debts. It’s usually met with lower interest rates, so it could save you money if you’re struggling to make multiple monthly payments. However, this method does come with substantial risk.

First, you could lose your home if you fail to make payments on the remortgage loan. And second, it’s not available to everyone—your credit score must be in good condition to qualify for this route. So, take a hard look at your finances before making this big decision.

How Does Debt Consolidation Affect Mortgage Loans?

Regardless of the consolidation method, the impacts of obtaining a mortgage loan can vary. In general, having consolidated debt could make it harder to qualify for a mortgage loan because of the temporary dip in your credit score. Additionally, lenders may view you as a risky borrower.

However, debt consolidation can be a red flag to some lenders, suggesting you have trouble managing your debt. This could disqualify you from getting the best interest rates and loan terms.

Why is Your Debt-to-income Ratio So Important?

One key factor in determining whether you’re eligible for a mortgage loan is your debt-to-income ratio. This percentage of your monthly gross income goes toward debt repayment. Lenders want to ensure you can afford to repay the loan, so a higher DTI could reduce your chances of approval.

Debt consolidation can impact your DTI ratio. If done correctly, it can lower your DTI, making you more attractive to mortgage lenders. However, if you accrue more debt after consolidating, your DTI could increase, which could jeopardize your chances of securing a home loan.

How to Prepare for a Home Purchase After Debt Consolidation?

To prepare for a home purchase after debt consolidation, it’s critical to maintain a good credit score and a low DTI ratio.

Maintaining a Healthy Credit Score

It’s important to know where you stand. Pull your credit report and scrutinize it for accuracy. Dispute any errors that may be present. Then, make sure to pay all your bills on time and maintain a low credit utilization rate (below 30%).

After consolidating your debts, staying disciplined with your new payment plan is essential. Make your payments on time, every time. Not only does this help you chip away at your debt, but it also shows potential lenders that you’re serious and reliable. And remember, good credit isn’t built overnight, so patience is key here.

Avoid Accumulating New Debt

After consolidating your debt, the last thing you want is to accumulate more debt. This includes putting large purchases on your credit card—even if you can pay off the balance immediately.

This might mean saying ‘no’ to tempting credit card offers or delaying big purchases until you can afford to pay for them outright. Adding more debt on top of what you’ve already consolidated could not only stress your budget but also negatively affect your credit score and ability to qualify for a home loan.

Saving For a Down Payment

Even with a mortgage, buying a home requires a sizable upfront payment: the down payment. The size of your down payment can affect the terms of your mortgage, including your interest rate and monthly payment.

While managing your consolidated debt, save for a down payment. Once you have enough, take some time to shop around and find the best loan options that fit your budget.

Understanding Your Budget

As you prepare for a home purchase after debt consolidation, take the time to understand your budget. Track your income and expenses, analyze where your money is going, and make adjustments if needed. This can help you find extra funds to save for a down payment, pay off debts faster, or increase your chances of qualifying for a loan.

Having a budget will help you avoid overextending yourself financially and ensure you can comfortably afford your new home without jeopardizing your debt payments or other financial responsibilities.

Shopping for a Good Mortgage

Once your credit score is solid, your debt is under control, and you’ve saved for a down payment, it’s time to start shopping for a mortgage. Do your research and compare different lenders, interest rates, and loan terms.

Pay attention to the fees associated with each option too. These fees can add up quickly, so ensure you understand each loan’s total cost.

FAQs

Does a consolidation loan stop you from getting a mortgage?

Not necessarily. A consolidation loan can improve your chances of getting a mortgage if it helps you manage your debt better, reduce your monthly payments, or lower your debt-to-income ratio. However, it can be negative if you accumulate more debt after consolidation or miss payments on your consolidation loan.

Are there any disadvantages to consolidating debt?

While there are benefits to debt consolidation, there can also be disadvantages. Also, consolidation methods, like balance transfers and debt relief services, could negatively impact your credit score.

What are the consequences of consolidating debt?

The consequences of consolidating debt can vary based on how you manage it. Debt consolidation can simplify your finances, reduce monthly payments, and improve your credit score, as long as it’s managed responsibly. However, if not managed properly, it can lead to a larger total debt, a lower credit score, and difficulty securing a mortgage.

Does debt consolidation go against you?

Debt consolidation doesn’t inherently go against you—it’s all about how you handle it. If managed properly, it can be a beneficial tool to simplify your financial management and potentially improve your credit standing. However, if you accumulate more debt after consolidation, miss payments, or choose a risky consolidation method, it could have negative effects on your financial health.

How many debts can I consolidate?

You can generally consolidate as many debts as you want. However, it’s important to keep in mind that consolidation works best if you have a manageable amount of debt. If you’re overwhelmed by debt, looking for other solutions, such as credit counseling, is probably best.

Conclusion

The question, “Does debt consolidation affect buying a home?” can be answered with a yes—but it’s not necessarily a negative effect. When managed correctly, debt consolidation can provide a way to streamline payments, lower monthly expenses, and potentially improve your credit score, all of which can help in securing a mortgage. However, it’s critical to remember that consolidation is not a cure-all for debt issues. After consolidation, good financial habits are still necessary to maintain a healthy debt-to-income ratio and credit score, helping pave the way toward homeownership.