")

Understanding Loan-to-Value (LTV) doesn’t have to be complicated. Whether you’re applying for a home loan, refinancing, or comparing mortgage options, knowing how to calculate LTV can help you make smarter financial decisions. Using a Loan-to-Value Ratio Calculator makes this process even easier by instantly showing the percentage of a property’s value that you’re borrowing.

Calculate your loan-to-value ratio

Existing mortgage information

LTV simply represents how much of a property’s value is financed through a loan, and lenders rely on it to assess risk, determine interest rates, and decide loan eligibility. In this guide, we’ll break down how to calculate Loan-to-Value in a clear, step-by-step way, explain why it matters, and show how a Loan-to-Value Ratio Calculator can impact your loan terms—so you can move forward with confidence.

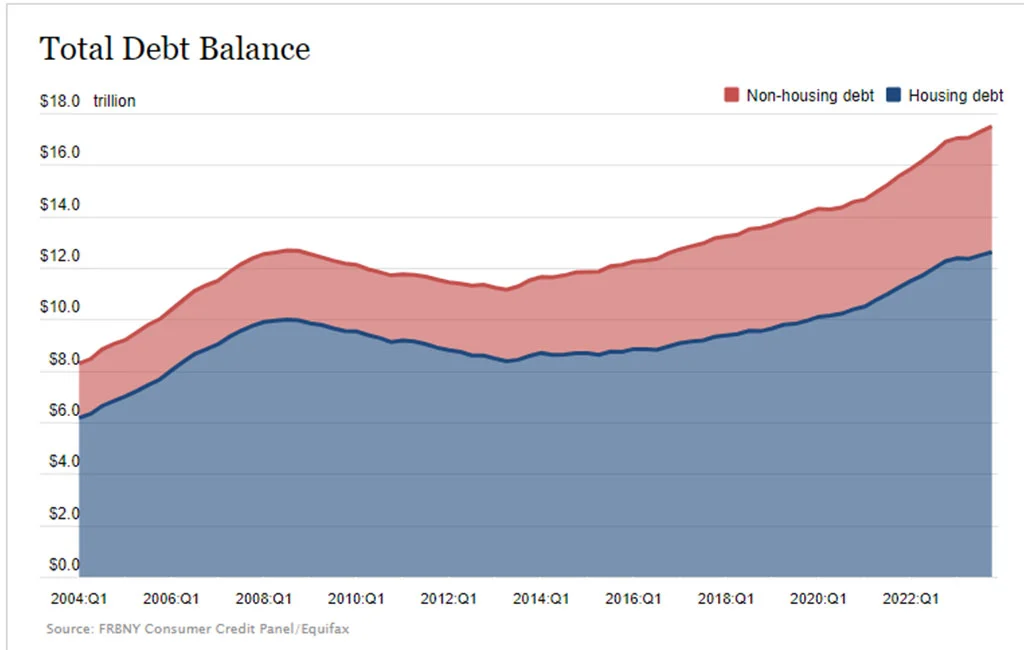

In the vast landscape of American finance, mortgages stand as the towering giants. With a staggering $12.61 trillion owed across 84 million mortgages, the average American with a mortgage is grappling with $145,000 of debt. This monumental figure isn’t just a number—it represents 70.3% of consumer debt in the US, highlighting the pivotal role of home loans in personal finance.

Navigating the world of finance, especially when it involves substantial commitments like loans, can be daunting. A fundamental concept that stands out in the process is the Loan-to-Value (LTV) ratio. Understanding and calculating this ratio is crucial for both lenders and borrowers, influencing decisions on loan approvals, interest rates, and terms. This comprehensive guide will cover the basic concepts of mortgage loans, how to calculate loan-to-value (LTV), and provide insights into its significance and implications.

What is the Loan-to-Value (LTV) Ratio?

The Loan-to-Value (LTV) ratio is a financial metric used by lenders to assess the risk of lending. It compares the loan amount to the value of the asset securing the loan. This ratio is a key factor in determining whether you get a mortgage, how you can refinance your existing mortgage, or if you can borrow against the equity in your home.

Understanding the LTV ratio is essential because it tells lenders how much risk they take by giving you a loan. Here’s how it works: Lenders see it as risky if you borrow nearly the full value of your home (meaning you have a high LTV ratio). They worry because they might not recover their money by selling the property if they fail to pay the loan. The reason? Your loan is almost as much as the property’s value, leaving little room for market fluctuations or sales costs.

A high LTV ratio signals lenders that you don’t have much equity in your property. Equity is the part of your home’s value that you truly “own” — the portion not tied up in loans. When equity is low, it means you haven’t paid off much of your home yet. If you default on your loan, the lender faces a tougher time getting their money back. They might not be able to sell the home for enough to cover what you owe, especially if market conditions aren’t great.

What is a Good Loan-to-Value?

A Loan-to-Value (LTV) ratio of 80% or less is best. Lenders see you as a safer bet and might get better loan deals, like lower interest rates. If your LTV ratio goes over 80%, borrowing costs can increase because lenders see it as risky. You might even need to buy private mortgage insurance, which is an extra cost.

When the LTV ratio hits 95% or more, it’s really risky for lenders. They usually don’t want to give loans with such a high LTV because if house prices drop, you could owe more than your house is worth. Keeping your LTV ratio at 80% or lower is a smart move to avoid extra costs and get good loan terms.

How to Calculate the Loan-to-Value Ratio

To find out how much equity you have in your home, start by taking the appraised value of your house. Then, subtract what you still owe on any loans that use your house as security. This means your main mortgage and any other loans like home equity or lines of credit with outstanding balances. Let’s use Ash as an example. Ash’s home is worth $400,000, and she owes $140,000 on her mortgage.

LTV = (Loan Amount/Asset Value) × 100

Next, to work out your Loan-to-Value (LTV) ratio, you’ll need to divide the amount you owe (this info is on your monthly mortgage statement or online) by the appraised value of your house. Turn that number into a percentage by multiplying it by 100. For Ash, when you divide $140,000 (what she owes) by $400,000 (her home’s value) and then multiply by 100, you find out Ash’s LTV ratio is 35%. This means Ash has borrowed 35% of her home’s value, showing she has a lot of equity.

Variations on Loan-to-Value (LTV) Ratio Rules

The Loan-to-Value (LTV) ratio is a financial metric used by lenders to assess the risk of lending. It compares the loan amount to the value of the asset securing the loan. This ratio is a key factor in determining whether you get a mortgage, how you can refinance your existing mortgage, or if you can borrow against the equity in your home.

Understanding the LTV ratio is essential because it tells lenders how much risk they take by giving you a loan. Here’s how it works: Lenders see it as risky if you borrow nearly the full value of your home (meaning you have a high LTV ratio). They worry because they might not recover their money by selling the property if they fail to pay the loan. The reason? Your loan is almost as much as the property’s value, leaving little room for market fluctuations or sales costs.

A high LTV ratio signals lenders that you don’t have much equity in your property. Equity is the part of your home’s value that you truly “own” — the portion not tied up in loans. When equity is low, it means you haven’t paid off much of your home yet. If you default on your loan, the lender faces a tougher time getting their money back. They might not be able to sell the home for enough to cover what you owe, especially if market conditions aren’t great.

So, in cases where foreclosure becomes a reality, a high LTV ratio can spell trouble for the lender. They risk losing money on the deal because selling the property might not bring in enough cash to pay off the outstanding mortgage and provide them with profit. This is why understanding and managing your LTV ratio is beneficial for both securing a loan and maintaining financial stability.

General Variations

When your Loan-to-Value (LTV) ratio is 80% or more, you usually have to buy PMI (Private Mortgage Insurance). This adds up to 1% more to your loan every year. Lenders don’t like LTV ratios of 95% or higher. But if your LTV ratio is 80% or less, you can skip buying PMI. Sometimes, if you make a lot of money, have little debt, or have a good investment income, lenders might make an exception.

Government LTV Rules

Even if you’re refinancing or need a loan for something else, your LTV ratio is important. The FHA (Federal Housing Administration) is okay with higher LTV ratios. Both the VA (Veterans Administration) and USDA (U.S. Department of Agriculture) give loans to military folks and people who are buying in rural areas without needing PMI. Fannie Mae and Freddie Mac help low-income borrowers get loans with LTV ratios up to 97%, but you’ll pay PMI until your LTV ratio is under 80%.

The CLTV Ratio

The CLTV (Combined Loan-to-Value) ratio considers all the loans on your property, making it a broader measure of risk. It includes your main mortgage, any second mortgage, home equity loans, credit lines, or other debts. If your CLTV ratio is over 80%, having a good credit score can help.

How LTV Affects Your Ability to Get a Home Loan

The LTV ratio is a critical factor in determining eligibility for a home loan. A high LTV ratio suggests a higher risk to the lender, which might result in higher interest rates, additional fees, or the requirement for mortgage insurance. Conversely, a lower LTV ratio increases the chances of loan approval under more favorable conditions.

LTV ratio is used within the mortgage loan consideration process:

- Determining Down Payments: The LTV ratio sets the required down payment amount for securing a loan. Essentially, the lower the LTV ratio, the larger the down payment a borrower has made, diminishing the loan amount needed from the lender.

- Influencing Interest Rates: Borrowers benefit from lower interest rates when they have a lower LTV ratio. A lower ratio reduces the lender’s risk, as much of the property’s price is already paid for.

- Affecting Financing Costs: Conversely, a higher LTV ratio indicates that the loan accounts for a greater share of the property’s value, increasing the risk for the lender. Higher financing costs for the borrower often compensate for this risk.

- Flexibility in Government Lending: Programs backed by the federal government tend to have more lenient LTV ratio requirements, making it easier for applicants to qualify for a loan even with higher LTV ratios.

- Requirement for PMI: For LTV ratios above a certain acceptable percentage, lenders usually require the purchase of Private Mortgage Insurance (PMI). This insurance safeguards the lender if the borrower defaults.

Loan-to-Value Rules for Different Mortgage Types

Lenders often specify the “maximum” Loan-to-Value (LTV) ratio for each of their loan offerings. The highest LTV ratios are usually available for purchasing a home or for rate-and-term refinancing, which aims to reduce your interest rate without withdrawing equity. For cash-out refinancing, where you take out cash based on your home’s equity, the maximum LTV ratios are typically lower.

Below is a guide to LTV ratio limits for common loan types, whether you’re buying or refinancing a single-family home:

| LTV Ratio Limits by Loan Type | ||

|---|---|---|

| Loan Type | Purpose | Max LTV |

| Conventional | Purchase | 97% |

| Cash-out refinance | 80% | |

| Rate-and-term refinance | 97% | |

| FHA | Purchase | 96.50% |

| Cash-out refinance | 80% | |

| Rate-and-term refinance | 97.75% | |

| VA | Purchase | 96.50% |

| Cash-out refinance | 90% | |

| Rate-and-term refinance | 100% | |

| USDA | Purchase | 100% |

| Cash-out refinance | Not allowed | |

| Rate-and-term refinance | 100% |

What Are the Disadvantages of Loan-to-Value?

While the LTV ratio is a useful tool for assessing loan risk, it has its limitations. High LTV ratios can lead to higher borrowing costs, including increased interest rates and insurance premiums. Understanding these disadvantages is crucial for managing your mortgage effectively and making informed decisions about borrowing and property investment.

- Higher Interest Rates and Costs: A high LTV ratio often leads to higher interest rates and borrowing costs. Lenders view loans with high LTV ratios as riskier, and they charge higher rates to offset this risk.

- Requirement for Private Mortgage Insurance (PMI): Borrowers with an LTV ratio above 80% typically need to purchase PMI. This insurance protects the lender in case of default but adds to the borrower’s monthly expenses.

- Limited Loan Options: Some loan programs have strict LTV ratio requirements. If your LTV ratio is too high, you might not qualify for the best loan terms or certain loan types at all.

- Difficulty Refinancing: If property values decrease and your LTV ratio increases (even beyond the original purchase LTV), refinancing can become challenging. Lenders might not approve refinancing applications for loans viewed as having too high a risk.

- Equity Building Slowdown: A high LTV ratio means you’re financing a larger portion of your property’s value. This can slow down the rate at which you build equity in your home, especially if property values remain stagnant or decline.

- Risk of Owing More Than the Home’s Worth: In a declining market, a high LTV ratio can quickly lead to a situation where you owe more on your mortgage than your home is currently worth, known as being “underwater” on your mortgage.

Final Words

Grasping the concept of how to calculate loan to value is essential for anyone involved in securing a loan. It not only influences the terms of the loan but also impacts the financial health of the borrower. By carefully considering the LTV ratio and striving for a lower percentage, borrowers can improve their loan conditions and navigate the path to financial security with greater confidence. Using a Loan-to-Value Ratio Calculator can further help borrowers quickly understand their borrowing position before applying for a loan.

FAQs

What is the formula for loan value?

The formula for calculating the LTV ratio is the loan amount divided by the asset’s value, multiplied by 100, to express it as a percentage. So, LTV = (Loan Amount/Asset Value) × 100.

What is an example of a loan to value?

Let’s say you put down $80,000 on a house worth $400,000. If you borrow $320,000, your LTV ratio is 80%. This ratio is typically within the range that most lenders find acceptable for home loans.

Why measure LTV?

Measuring the LTV ratio helps lenders assess the risk associated with a loan. It determines the likelihood of loan approval, interest rates, and necessary insurance. Typically lenders prefer an LTV value below 80%.

Is higher LTV better?

No, higher LTV is not good. Generally, a lower LTV is preferable as it indicates less risk for the lender and can lead to better loan terms for the borrower. Higher LTV ratios may require additional costs, such as mortgage insurance.

How do you calculate 80% LTV?

To calculate an 80% Loan-to-Value (LTV) ratio, you start by understanding that LTV compares the mortgage amount to the home’s appraised value. For example, if you make a down payment of 20% on a home priced at $300,000, that’s a $60,000 down payment. This leaves $240,000 remaining as the mortgage debt on the home. Therefore, the LTV ratio, which measures this remaining debt against the home’s value, would be 80%.