In the landscape of retirement planning, one question often floats to the surface: Is a 401K worth it? The answer isn’t straightforward because individual financial situations vary. Still, it’s essential to understand the overarching benefits and limitations of a 401(k) to make an informed decision.

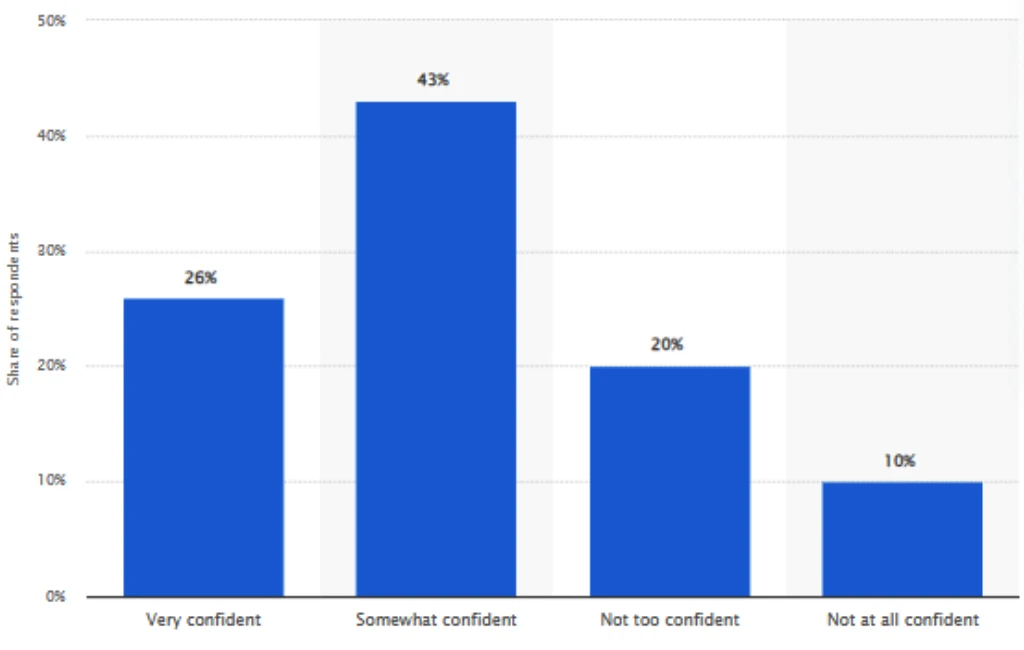

In a world where financial uncertainty often reigns, a silver lining emerged from a 2022 survey in the United States. A striking 69 percent of workers expressed confidence in their financial preparation for retirement, showcasing an uplifting trend in proactive financial planning.

This heartening statistic not only underscores the rising awareness about retirement readiness but also hints at a potentially brighter financial future for many. But what drives this newfound confidence? Let’s delve deeper into retirement planning and the factors influencing such optimism.

Why Retirement Savings Matter

Before jumping into the specifics of a 401(k), it’s critical to grasp the importance of retirement savings. We live in an age where the future of social security is uncertain, and pension plans are becoming rarer. Having a nest egg means financial independence, reduced stress about outliving your savings, and the ability to pursue hobbies, travel, or even assist the next generation.

The Uncertainty of the Future: Predicting the Unpredictable

While life is filled with unforeseen twists and turns, especially concerning career paths, family dynamics, and broader social support systems, it’s vital to carve out areas of predictability. Retirement savings stand as one of those few certainties, acting as a buffer against the capriciousness of the future, ensuring that no matter the external changes, there remains a stable financial foundation.

The Decline of Pensions: No Longer the Norm

The golden era of employer-supported pensions has waned. Today, only a handful of industries still offer this cherished safety net. This shift places the onus on individuals to be proactive in securing their retirement. The absence of these once-standard benefits underlines the criticality of personal savings in achieving a comfortable retirement.

The Power of Self-Reliance: Crafting Your Financial Destiny

While everyone dreams of striking gold or hitting the jackpot, banking on such unpredictable events is not a viable retirement strategy. Instead, cultivating a mindset of self-reliance and taking deliberate steps toward saving allows individuals to craft their financial destiny, ensuring they’re not merely at the mercy of chance but are steering the ship of their future.

The Magic of Compound Interest: Letting Time Work For You

One of the most potent tools in retirement savings is compound interest. It’s not just about the money saved today but also the interest it will earn over time. Savings grow exponentially when interest is earned on both the initial amount saved and the interest it has already accrued. This ‘interest on interest‘ effect means that every dollar saved today has the potential to multiply manifold, letting time and mathematics work in favor of a secure retirement.

What Are the Advantages of a 401(k)?

A 401(k) plan is an employer-sponsored retirement savings vehicle that comes with numerous benefits:

Tax Benefits

Think of a 401(k) as a special savings jar where the money you put in isn’t immediately taxed by the government. This means you can save more of your paycheck now. Plus, the money inside this jar grows without being taxed until you decide to use it during retirement.

Employer Match

Imagine if someone added a bit more on top every time you put a dollar into your savings – that’s what an employer match does– Free Money! Many companies offer to match a part of what you save in your 401(k), giving you free retirement money.

High Contribution Limits

A 401(k) is like a big retirement piggy bank. Compared to other savings options, you can put a lot more money into a 401(k) each year. This lets you save more and ensures your money keeps growing over time.

Automatic Deductions

Setting aside money can be hard, but it’s easier with a 401(k). A specific amount is automatically taken from your paycheck and added to your retirement savings before seeing it. It’s a hassle-free way of ensuring you’re consistently saving for your future.

Is It Better to Have a 401(k) or an IRA?

Deciding between a 401(k) and an Individual Retirement Account (IRA) can feel like comparing apples to oranges. Both are powerful tools in the arsenal of retirement planning, but they serve different needs and come with distinct features. Let’s delve deeper into their differences:

Contribution Limits: Every year, you can contribute a maximum amount of money to retirement accounts. Here’s where 401(k)s have an edge. They allow you to put away a more substantial sum each year than IRAs. This might be particularly beneficial for those aiming to maximize their retirement savings or those who start saving a bit later in their careers and want to catch up quickly.

Taxation: How your money is taxed can significantly impact how much you have when you retire. Both traditional 401(k)s and IRAs offer what’s known as “tax-deferred” growth. Simply put, you don’t pay taxes on the money you put in or its gains until you withdraw it in retirement. On the other hand, Roth IRAs and Roth 401(k)s are a bit different. With these accounts, you pay taxes on your money before you deposit it, but the big perk comes later: you can withdraw your savings and earnings tax-free in retirement. This can be a significant advantage, especially if you expect to be in a higher tax bracket in your golden years.

Flexibility: While a 401(k) often comes with the benefit of an employer match, it may also have limitations, especially regarding investment choices. Most 401(k) plans offer a select list of investment options the employer or plan provider curated. IRAs, in contrast, typically offer a broader range of investment choices, giving savers more flexibility to diversify and tailor their portfolios according to their risk tolerance and financial goals. An IRA might appeal more to those who like to have more control and variety in their investment strategy.

Consider an IRA Instead

An IRA might be a better choice for those who want greater investment flexibility or are self-employed. It’s also worth considering if your employer doesn’t offer a 401(k) match or if you’ve maxed out your 401(k) contributions for the year.

IRAs stand out for their broad investment choices, allowing for a diversified and tailored portfolio. Unlike the often limited options of a 401(k), an IRA empowers individuals with a more versatile range, catering to varied financial strategies and risk profiles.

With the rise of freelancing and entrepreneurship, not everyone can access a 401(k). For the self-employed, IRAs, particularly SEP-IRA or SIMPLE IRA, offer a fitting solution, providing tax benefits and flexibility tailored to their unique needs.

While 401(k)s often come with the allure of employer matches, not every employer offers this. In such cases, or if one hits the annual contribution limit of a 401(k), IRAs serve as an appealing alternative, enabling continued tax-advantaged savings and growth potential.

Risks and Drawbacks of 401(k) Plans

While 401(k) plans offer numerous benefits, there are some potential pitfalls:

Limited Investment Choices

One of the often-cited drawbacks of many 401(k) plans is their limited selection of investment options. Unlike IRAs, which typically provide a wider array of investment opportunities, 401(k)s are often restricted to a pre-selected list of funds curated by the plan provider. This limitation might not cater to all investors, especially those who wish for a more diversified or tailored investment strategy.

Fees

Hidden beneath the surface of some 401(k) plans are a myriad of fees. These can include administrative fees, investment fees, and service charges. Over time, even seemingly small fees can eat away at an investor’s returns. Participants must be aware of and understand these fees, as they can significantly impact the overall growth of the retirement nest egg.

Penalties

While 401(k) plans encourage long-term savings for retirement, they’re not very forgiving when it comes to early withdrawals. Taking money out before age usually triggers a 10% penalty in addition to regular income taxes. Such penalties can severely hamper the growth potential of the saved amount and should be a key consideration for those thinking of accessing their funds prematurely.

Lack of Liquidity

By design, 401(k) accounts are meant to be long-term savings vehicles. Accessing funds can be more challenging than other investment or savings accounts. While there are provisions for hardship withdrawals or loans against 401(k) balances, they come with rules and potential consequences, making the funds less liquid than some might desire.

Dependence on Employer's Financial Health

In instances where employers match contributions, the vested interest might depend on a certain tenure or the company’s financial health. If a company faces financial difficulties or goes bankrupt, it could affect the vesting schedule or even the availability of previously promised matching funds, which could, in turn, impact an employee’s overall retirement savings strategy.

Retirement is One Goal of Many

In the grand tapestry of life’s financial journey, retirement emerges as a significant milestone, demanding foresight, planning, and consistent savings. However, life is multi-faceted, and the path to retirement is punctuated with other equally vital financial markers. Purchasing a dream home, ensuring quality education for oneself or family, or even fulfilling desires like traveling the world all come with financial commitments.

Moreover, the unpredictable twists of life might introduce unexpected expenses or the need for emergency funds. Consequently, while the tranquility of a secured retirement beckons, it’s essential not to view it in isolation.

It must uphold other pressing financial objectives as critical as building that retirement nest egg. For many, grappling with student loans, credit card debt, or mortgages becomes a priority to secure a stable financial foundation. Others might prioritize investing in their children’s education or launching a business venture. Striking the right balance involves comprehensive financial planning.

This means creating a diversified strategy that allocates resources towards a comfortable retirement and addresses immediate and intermediate financial goals. Maintaining such a holistic view ensures a well-rounded financial journey characterized by preparedness and fulfillment at every stage.

Final Words

As we explore the question, “Is a 401K worth it?”, we find that, for many, the benefits of tax advantages, employer matching, and disciplined saving make it an attractive option. However, as with all financial decisions, it’s crucial to assess individual circumstances and consult a financial advisor to make the best choice for your future.

At EduCounting, our mission is to empower the youth with financial literacy and effective money management techniques. Dive into our plethora of educational resources and tools designed to give you the reins of your financial journey. Enroll in our complimentary course and pave your way to mastering money management!

FAQs

What is the downside of a 401k?

The most significant downsides include limited investment choices, potential high fees, and penalties for early withdrawal.

Is it better to save money or 401k?

It’s essential to have an emergency fund in liquid savings. Beyond that, taking advantage of a 401(k), especially if there’s an employer match, can offer greater long-term growth and tax advantages.

Is it smart to put money in a 401k?

Generally, yes. A 401(k) provides tax advantages, potential employer matching and allows for automatic savings. However, always consider your unique financial situation and goals.